NZ IAS 21

The Effects of Changes in Foreign Exchange Rates

Statement of Authority

![]()

New Zealand Equivalent to International Accounting Standard 21 The Effects of Changes in Foreign Exchange Rates (NZ IAS 21)

Issued November 2004 and incorporates amendments to 28 February 2024

This Standard was issued by the New Zealand Accounting Standards Board of the External Reporting Board pursuant to section 24(1)(a) of the Financial Reporting Act 1993.

This Standard is a Regulation for the purposes of the Regulations (Disallowance) Act 1989.

NZ IAS 21 incorporates the equivalent IFRS® Standard as issued by the International Accounting Standards Board (IASB).

Tier 1 for-profit entities that comply with NZ IAS 21 will simultaneously be in compliance with IAS 21 The Effects of Changes in Foreign Exchange Rates.

NZ IAS 21 includes RDR disclosure concessions and associated RDR paragraphs for entities that qualify for and elect to apply Tier 2 for-profit accounting requirements in accordance with XRB A1 Application of the Accounting Standards Framework. Entities that elect to report in accordance with Tier 2 accounting requirements are not required to comply with paragraphs in this Standard denoted with an asterisk (*). However, an entity is required to comply with any RDR paragraph associated with a disclosure concession that is adopted.

Copyright

© External Reporting Board (XRB) 2011

This XRB standard contains International Financial Reporting Standards (IFRS®) Foundation copyright

Requests and enquiries concerning reproduction and rights for commercial purposes within New Zealand should be addressed to the Chief Executive, External Reporting Board at the following email address: enquiries@xrb.govt.nz and the IFRS Foundation at the following email address: permissions@ifrs.org.

All existing rights (including copyrights) in this

ISBN 1-877430-31-5

Copyright

IFRS Standards are issued by the International Accounting Standards Board

Columbus Building, 7 Westferry Circus, Canary Wharf, London, E14 4HD, United Kingdom. Tel: +44 (0)20 7246 6410

Email: info@ifrs.org Web: www.ifrs.org

Copyright © International Financial Reporting Standards Foundation All rights reserved. Reproduced and distributed by the External Reporting Board with the permission of the IFRS Foundation. This English language version of the IFRS Standards is the copyright of the IFRS Foundation.

1. The IFRS Foundation grants users of the English language version of IFRS Standards (Users) the permission to reproduce the IFRS Standards for

-

the User’s Professional Use, or

-

private study and education

Professional Use: means use of the English language version of the IFRS Standards in the User’s professional capacity in connection with the

For the avoidance of doubt, the abovementioned usage does not include any kind of activities that make (commercial) use of the IFRS Standards other than direct or indirect application of IFRS Standards, such as but not limited to commercial seminars, conferences, commercial training or similar events.

2. For any application that falls outside Professional Use, Users shall be obliged to contact the IFRS Foundation for a separate individual licence under terms and conditions to be mutually agreed.

3. Except as otherwise expressly permitted in this notice, Users shall not, without prior written permission of the Foundation have the right to license, sublicense, transmit, transfer, sell, rent, or otherwise distribute any portion of the IFRS Standards to third parties in any form or by any means, whether electronic, mechanical or otherwise either currently known or yet to be invented.

4. Users are not permitted to modify or make alterations, additions or amendments to or create any

5. Commercial reproduction and use rights are strictly prohibited. For further information please contact the IFRS Foundation at permissions@ifrs.org.

The authoritative text of IFRS Standards is that issued by the International Accounting Standards Board in the English language. Copies may be obtained from the IFRS Foundation’s Publications Department.

Please address publication and copyright matters in English to:

IFRS Foundation Publications Department

Columbus Building, 7 Westferry Circus, Canary Wharf, London, E14 4HD, United Kingdom. Tel: +44 (0)20 7332 2730 Fax: +44 (0)20 7332 2749

Email: publications@ifrs.org Web: www.ifrs.org

Trade Marks

![]()

The IFRS Foundation logo, the IASB logo, the IFRS for SMEs logo, the “Hexagon Device”, “IFRS Foundation”, “eIFRS”, “IAS”, “IASB”, “IFRS for SMEs”, “IASs”, “IFRS”, “IFRSs”, “International Accounting Standards” and “International Financial Reporting Standards”, “IFRIC” and “SIC” are Trade Marks of the IFRS Foundation.

Disclaimer

The authoritative text of the IFRS Standards is reproduced and distributed by the External Reporting Board in respect of their application in New Zealand. The International Accounting Standards Board, the Foundation, the authors and the publishers do not accept responsibility for loss caused to any person who acts or refrains from acting in reliance on the

How to read this Standard

New Zealand Equivalent to International Accounting Standard 21 The Effects of Changes in Foreign Exchange Rates (NZ IAS 21) is set out in paragraphs 1–62 and the Appendix. NZ IAS 21 is based on International Accounting Standard 21 The Effects of Changes in Foreign Exchange Rates (IAS 21) (2003) initially issued by the International Accounting Standards Committee (IASC) and subsequently revised by the International Accounting Standards Board (IASB). All the paragraphs have equal authority but retain the IASC format of the Standard. NZ IAS 21 should be read in the context of its objective and the IASB’s Basis for Conclusions on IAS 21 and the New Zealand Equivalent to the IASB Conceptual Framework for Financial Reporting. NZ IAS 8

Any New Zealand additional

-

in accounting for transactions and balances in foreign currencies, except for those

derivative transactions and balances that are within the scope of NZ IFRS 9 Financial Instruments; -

in translating the results and financial position of foreign operations that are included in the financial statements of the entity by consolidation or the

equity method -

in translating an entity’s results and financial position into a

presentation currency .

A currency is exchangeable into another currency when an entity is able to obtain the other currency within a time frame that allows for a normal administrative delay and through a market or exchange mechanism in which an exchange transaction would create enforceable rights and obligations.

A

Elaboration on the definitions

Exchangeable (paragraphs A2–A10)

-

at a

measurement date -

for a specified purpose.

Functional currency

-

the currency:

-

that mainly influences sales prices for goods and services (this will often be the currency in which sales prices for its goods and services are denominated and settled); and

-

of the country whose competitive forces and regulations mainly determine the sales prices of its goods and services.

-

-

the currency that mainly influences labour,

material and other costs of providing goods or services (this will often be the currency in which such costs are denominated and settled).

-

the currency in which funds from

financing activities (ie issuing debt andequity instruments) are generated. -

the currency in which receipts from

operating activities are usually retained.

-

whether the activities of the

foreign operation are carried out as an extension of thereporting entity , rather than being carried out with a significant degree of autonomy. An example of the former is when theforeign operation only sells goods imported from thereporting entity and remits the proceeds to it. An example of the latter is when the operation accumulatescash and othermonetary items , incursexpenses , generatesincome and arranges borrowings, all substantially in its local currency. -

whether transactions with the

reporting entity are a high or a low proportion of theforeign operation ’s activities. -

whether

cash flows from the activities of theforeign operation directly affect thecash flows of thereporting entity and are readily available for remittance to it. -

whether

cash flows from the activities of theforeign operation are sufficient to service existing and normally expected debt obligations without funds being made available by thereporting entity .

Net investment in a foreign operation

Monetary items

Initial recognition

-

buys or sells goods or services whose price is denominated in a

foreign currency ; -

borrows or lends funds when the amounts payable or receivable are denominated in a

foreign currency ; or -

otherwise acquires or disposes of assets, or incurs or settles liabilities, denominated in a

foreign currency .

Reporting at the end of the subsequent reporting periods

-

foreign currency monetary items shall be translated using theclosing rate ; -

non-

monetary items that are measured in terms of historicalcost in aforeign currency shall be translated using theexchange rate at the date of the transaction; and -

non-

monetary items that are measured atfair value in aforeign currency shall be translated using the exchange rates at the date when thefair value was measured.

-

the

cost orcarrying amount , as appropriate, translated at theexchange rate at the date when that amount was determined (ie the rate at the date of the transaction for an item measured in terms of historicalcost ); and -

the

net orrealisable value recoverable amount , as appropriate, translated at theexchange rate at the date when that value was determined (eg theclosing rate at the end of the reporting period).

The effect of this comparison may be that an

Recognition of exchange differences

Change in functional currency

Translation to the presentation currency

-

assets and liabilities for each statement of financial position presented (ie including comparatives) shall be translated at the

closing rate at the date of that statement of financial position; -

income andexpenses for each statement presentingprofit or loss andother comprehensive (ie including comparatives) shall be translated at exchange rates at the dates of the transactions; andincome -

all resulting exchange differences shall be recognised in

other comprehensive .income

-

translating

income andexpenses at the exchange rates at the dates of the transactions and assets and liabilities at theclosing rate . -

translating the opening net assets at a

closing rate that differs from the previousclosing rate .

These exchange differences are not recognised in

-

all amounts (ie assets, liabilities,

equity items,income andexpenses , including comparatives) shall be translated at theclosing rate at the date of the most recent statement of financial position, except that -

when amounts are translated into the currency of a non-hyperinflationary economy, comparative amounts shall be those that were presented as current year amounts in the relevant prior year financial statements (ie not adjusted for subsequent changes in the price level or subsequent changes in exchange rates).

Translation of a foreign operation

Disposal or partial disposal of a foreign operation

-

when the partial disposal involves the loss of control of a

subsidiary that includes aforeign operation , regardless of whether the entity retains anon-controlling interest in its formersubsidiary after the partial disposal; and -

when the retained interest after the partial disposal of an interest in a

joint arrangement or a partial disposal of an interest in anassociate that includes aforeign operation is afinancial that includes aasset foreign operation . -

[deleted by IASB]

-

the amount of exchange differences recognised in

profit or loss except for those arising on financial instruments measured atfair value throughprofit or loss in accordance with NZ IFRS 9; and -

net exchange differences recognised in

other comprehensive and accumulated in a separate component ofincome equity , and a reconciliation of the amount of such exchange differences at the beginning and end of the period.

-

clearly identify the information as supplementary information to distinguish it from the information that complies with IFRSs;

-

disclose the currency in which the supplementary information is displayed; and

-

disclose the entity’s

functional currency and the method of translation used to determine the supplementary information.

-

the nature and financial effects of the currency not being exchangeable into the other currency;

-

the

spot (s) used;exchange rate -

* the estimation process; and

-

* the risks to which the entity is exposed because of the currency not being exchangeable into the other currency.

Lack of Exchangeability

-

when the entity reports

foreign currency transactions in itsfunctional currency , and, at the date of initial application, concludes that itsfunctional currency is not exchangeable into theforeign currency or, if applicable, concludes that theforeign currency is not exchangeable into itsfunctional currency , the entity shall, at the date of initial application:-

translate affected

foreign currency monetary items , and non-monetary items measured atfair value in aforeign currency , using the estimatedspot at that date; andexchange rate -

recognise any effect of initially applying the amendments as an adjustment to the opening balance of retained earnings.

-

-

when the entity uses a

presentation currency other than itsfunctional currency , or translates the results and financial position of aforeign operation , and, at the date of initial application, concludes that itsfunctional currency (or theforeign operation ’sfunctional currency ) is not exchangeable into itspresentation currency or, if applicable, concludes that itspresentation currency is not exchangeable into itsfunctional currency (or theforeign operation ’sfunctional currency ), the entity shall, at the date of initial application:-

translate affected assets and liabilities using the estimated

spot at that date;exchange rate -

translate affected

equity items using the estimatedspot at that date if the entity’sexchange rate functional currency is hyperinflationary; and -

recognise any effect of initially applying the amendments as an adjustment to the cumulative amount of translation differences—accumulated in a separate component of

equity .

-

When amending Standard takes effect (section 27 Financial Reporting Act 2013)

Accounting period in relation to which standards commence to apply (section 28 Financial Reporting Act)

-

for an early adopter, those accounting periods following and including, the early adoption accounting period.

-

for any other

reporting entity , those accounting periods following, and including, the first accounting period for the entity that begins on or after the mandatory date.

early adopter means a

early adoption accounting period means an accounting period of the early adopter:

-

that begins before the mandatory date but has not ended or does not end before this amending Standard takes effect (and to avoid doubt, that period may have begun before this amending Standard takes effect); and

-

for which the early adopter:

-

first applies this amending Standard in preparing its financial statements; and

-

discloses in its financial statements for that accounting period that this amending Standard has been applied for that period.

-

mandatory date means 1 January 2025.

Lack of Exchangeability RDR

When amending Standard takes effect (section 27 Financial Reporting Act 2013)

Accounting period in relation to which standards commence to apply (section 28 Financial Reporting Act)

-

for an early adopter, those accounting periods following and including, the early adoption accounting period.

-

for any other

reporting entity , those accounting periods following, and including, the first accounting period for the entity that begins on or after the mandatory date.

early adopter means a

early adoption accounting period means an accounting period of the early adopter:

-

that begins before the mandatory date but has not ended or does not end before this amending Standard takes effect (and to avoid doubt, that period may have begun before this amending Standard takes effect); and

-

for which the early adopter:

-

first applies this amending Standard in preparing its financial statements; and

-

discloses in its financial statements for that accounting period that this amending Standard has been applied for that period.

-

mandatory date means 1 January 2025.

This appendix is an integral part of the Standard.

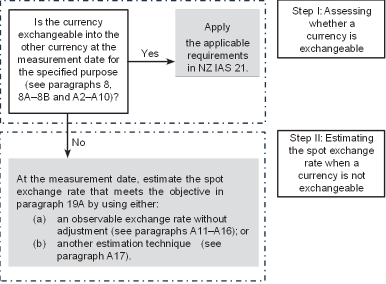

Step I: Assessing whether a currency is exchangeable (paragraphs 8 and 8A–8B)

Time frame

Ability to obtain the other currency

Markets or exchange mechanisms

Purpose of obtaining the other currency

-

set a preferential

exchange rate for imports of those goods and a ‘penalty’exchange rate for capital remittances to other jurisdictions, thus resulting in different exchange rates applying to different exchange transactions; or -

make the other currency available only to pay for imports of those goods and not for capital remittances to other jurisdictions.

-

when an entity reports

foreign currency transactions in itsfunctional currency (see paragraphs 20– 37), the entity shall assume its purpose in obtaining the other currency is to realise or settle individualforeign currency transactions, assets or liabilities. -

when an entity uses a

presentation currency other than itsfunctional currency (see paragraphs 38–43), the entity shall assume its purpose in obtaining the other currency is to realise or settle its net assets or net liabilities. -

when an entity translates the results and financial position of a

foreign operation into thepresentation currency (see paragraphs 44–47), the entity shall assume its purpose in obtaining the other currency is to realise or settle its net investment in theforeign operation .

-

the distribution of a financial return to the entity’s

owners ; -

the receipt of a financial return from the entity’s

foreign operation ; or -

the recovery of the investment by the entity or the entity’s

owners , such as through disposal of the investment.

Ability to obtain only limited amounts of the other currency

Step II: Estimating the spot exchange rate when a currency is not exchangeable (paragraph 19A)

Using an observable exchange rate without adjustment

-

a

spot for a purpose other than that for which an entity assesses exchangeability (see paragraphs A13–A14); andexchange rate -

the first

exchange rate at which an entity is able to obtain the other currency for the specified purpose after exchangeability of the currency is restored (first subsequentexchange rate ) (see paragraphs A15–A16).

Using an observable exchange rate for another purpose

-

whether several observable exchange rates exist—the existence of more than one observable

exchange rate might indicate that exchange rates are set to encourage, or deter, entities from obtaining the other currency for particular purposes. These observable exchange rates might include an ‘incentive’ or ‘penalty’ and therefore might not reflect the prevailing economic conditions. -

the purpose for which the currency is exchangeable—if an entity is able to obtain the other currency only for limited purposes (such as to import emergency supplies), the observable

exchange rate might not reflect the prevailing economic conditions. -

the nature of the

exchange rate —a free-floating observableexchange rate is more likely to reflect the prevailing economic conditions than anexchange rate set through regular interventions by the relevant authorities. -

the frequency with which exchange rates are updated—an observable

exchange rate unchanged over time is less likely to reflect the prevailing economic conditions than an observableexchange rate that is updated on a daily basis (or even more frequently).

Using the first subsequent exchange rate

-

the time between the

measurement dateexchange rate will reflect the prevailing economic conditions. -

inflation rates—when an economy is subject to high inflation, including when an economy is hyperinflationary (as specified in NZ IAS 29 Financial Reporting in Hyperinflationary Economies), prices often change quickly, perhaps several times a day. Accordingly, the first subsequent

exchange rate for a currency of such an economy might not reflect the prevailing economic conditions.

Using another estimation technique

Disclosure when a currency is not exchangeable

-

the currency and a description of the restrictions that result in that currency not being exchangeable into the other currency;

-

a description of affected transactions;

-

the

carrying amount of affected assets and liabilities; -

the spot exchange rates used and whether those rates are:

-

observable exchange rates without adjustment (see paragraphs A12–A16); or

-

spot exchange rates estimated using another estimation technique (see paragraph A17);

-

-

* a description of any estimation technique the entity has used, and qualitative and quantitative information about the

inputs and assumptions used in that estimation technique; and -

* qualitative information about each type of risk to which the entity is exposed because the currency is not exchangeable into the other currency, and the nature and

carrying amount of assets and liabilities exposed to each type of risk.

-

the name of the

foreign operation ; whether theforeign operation is asubsidiary ,joint operation ,joint venture ,associate or branch; and its principal place ofbusiness ; -

summarised financial information about the

foreign operation ; and -

* the nature and terms of any contractual arrangements that could require the entity to provide financial support to the

foreign operation , including events or circumstances that could expose the entity to a loss.

The amendments in this appendix shall be applied for annual periods beginning on or after 1 January 2005. If an entity applies this Standard for an earlier period, these amendments shall be applied for that earlier period.

*****

The amendments contained in this appendix have been incorporated into the relevant pronouncements.

Table of Pronouncements – NZ IAS 21 The Effects of Changes in Foreign Exchange Rates

This table lists the pronouncements establishing and substantially amending NZ IAS 21. The table is based on amendments approved as at 28 February 2024.

|

Pronouncements |

Date issued |

Early operative date |

Mandatory date (annual reporting periods… on or after …) |

|

NZ IAS 21 The Effects of Changes in Foreign Exchange Rates |

Nov 2004 |

1 Jan 2005 |

1 Jan 2007 |

|

Amendment to NZ IAS 21: |

Feb 2006 |

1 Jan 2006 |

1 Jan 2007 |

|

NZ IAS 1 Presentation of Financial Statements (revised 2007) |

Nov 2007 |

Early application permitted |

1 Jan 2009 |

|

NZ IAS 27 Consolidated and |

Feb 2008 |

Early application permitted |

I July 2009 |

|

Amendments to NZ IFRS 1 and NZ IAS 27— |

June 2008 |

Early application permitted |

1 Jan 2009 |

|

NZ IFRS 9 Financial Instruments (2009) |

Nov 2009 |

Early application permitted |

1 Jan 20131 |

|

Improvements to NZ IFRSs |

July 2010 |

Early application permitted |

1 July 2010 |

|

Minor Amendments to NZ IFRSs |

July 2010 |

Immediate |

Immediate |

|

NZ IFRS 9 Financial Instruments (2010) |

Nov 2010 |

Early application permitted |

1 Jan 20132 |

|

NZ IFRS 10 |

June 2011 |

Early application permitted |

1 Jan 2013 |

|

NZ IFRS 11 Joint Arrangements |

June 2011 |

Early application permitted |

1 Jan 2013 |

|

NZ IFRS 13 |

June 2011 |

Early application permitted |

1 Jan 2013 |

|

Presentation of Items of (Amendments to NZ IAS 1) |

Aug 2011 |

Early application permitted |

1 July 2012 |

|

Framework: Tier 1 and Tier 2 For-profit Entities3 |

Nov 2012 |

Early application permitted |

1 Dec 2012 |

|

NZ IFRS 9 Financial Instruments (2013) (Hedge Accounting and Amendments to NZ IFRS 9, NZ IFRS 7 and NZ IAS 39) |

Dec 2013 |

Early application permitted |

1 Jan 20174 |

|

NZ IFRS 9 Financial Instruments (2014) |

Sept 2014 |

Early application permitted |

1 Jan 2018 |

|

2017 Omnibus Amendments to NZ IFRS (editorial corrections only) |

Nov 2017 |

Early application permitted |

1 Jan 2018 |

|

NZ IFRS 16 Leases |

Feb 2016 |

Early application permitted |

1 Jan 2019 |

|

Lack of Exchangeability |

Nov 2023 |

Early application permitted |

1 Jan 2025 |

|

Lack of Exchangeability RDR |

Jan 2024 |

Early application permitted |

1 Jan 2025 |

Table of Amended Paragraphs in NZ IAS 21

|

Paragraph affected |

How affected |

By … [date] |

|

Amended |

NZ IFRS 11 [June 2011] |

|

|

Amended |

NZ IFRS 9 (2009) [Nov 2009], NZ IFRS 9 (2010 [Nov 2010], NZ IFRS 9 (2013) [Dec 2013] and NZ IFRS 9 (2014) [Sept 2014] |

|

|

Added |

Presentation of Items of |

|

|

Amended |

NZ IFRS 9 (2009) [Nov 2009], NZ IFRS 9 (2010 [Nov 2010], NZ IFRS 9 (2013) [Dec 2013] and NZ IFRS 9 (2014) [Sept 2014] |

|

|

Amended |

NZ IFRS 9 (2013) [Dec 2013] and NZ IFRS 9 (2014) [Sept 2014] |

|

|

Amended |

NZ IFRS 11 [June 2011] |

|

|

Amended |

Lack of Exchangeability [Nov 2023] |

|

|

Paragraph 8A and preceding heading |

Added |

Lack of Exchangeability [Nov 2023] |

|

Added |

Lack of Exchangeability [Nov 2023] |

|

|

Amended |

NZ IFRS 11 [June 2011] |

|

|

Added |

Amendment to NZ IAS 21 [Feb 2006] |

|

|

Amended |

NZ IFRS 16 [Feb 2016] |

|

|

Amended |

NZ IFRS 11 [June 2011] |

|

|

Amended |

NZ IFRS 10 [June 2011] |

|

|

Paragraph 19A and preceding heading |

Added |

Lack of Exchangeability [Nov 2023] |

|

Amended |

NZ IFRS 13 [June 2011] |

|

|

Amended |

Lack of Exchangeability [Nov 2023] |

|

|

Amended |

NZ IAS 1 [Nov 2007] |

|

|

Amended |

NZ IFRS 9 (2013) [Dec 2013] and NZ IFRS 9 (2014) [Sept 2014] |

|

|

Amended |

NZ IAS 1 [Nov 2007] |

|

|

Amended |

NZ IAS 1 [Nov 2007] |

|

|

Amended |

NZ IAS 1 [Nov 2007] |

|

|

Amended |

Amendment to NZ IAS 21 [Feb 2006] |

|

|

Amended |

NZ IAS 1 [Nov 2007] |

|

|

Amended |

NZ IFRS 11 [June 2011] |

|

|

Amended |

NZ IAS 1 [Nov 2007] |

|

|

Amended |

NZ IAS 1 [Nov 2007] |

|

|

Amended |

Presentation of Items of |

|

|

Amended |

NZ IAS 1 [Nov 2007] |

|

|

Amended |

NZ IAS 1 [Nov 2007] |

|

|

Amended |

NZ IFRS 11 [June 2011] |

|

|

Amended |

NZ IFRS 10 and NZ IFRS 11 [June 2011] |

|

|

Amended |

NZ IFRS 10 and NZ IFRS 11 [June 2011] |

|

|

Heading preceding paragraph 48 |

Amended |

NZ IAS 27 [Feb 2008] |

|

Amended |

NZ IAS 1 [Nov 2007] |

|

|

Paragraphs 48A–48D |

Added |

NZ IAS 27 [Feb 2008] |

|

Amended |

NZ IFRS 11 [June 2011] |

|

|

Amended |

NZ IAS 27 [Feb 2008] |

|

|

Amended |

||

|

Amended |

NZ IAS 1 [Nov 2007] |

|

|

Amended |

NZ IFRS 9 (2009) [Nov 2009], NZ IFRS 9 (2010 [Nov 2010], NZ IFRS 9 (2013) [Dec 2013] and NZ IFRS 9 (2014) [Sept 2014] |

|

|

Added |

Lack of Exchangeability [Nov 2023] |

|

|

Amended |

Lack of Exchangeability RDR [Jan 2024] |

|

|

Added |

Lack of Exchangeability [Nov 2023] |

|

|

Added |

Amendment to NZ IAS 21 [Feb 2006] |

|

|

Added |

NZ IAS 1 [Nov 2007] |

|

|

Added |

NZ IAS 27 [Feb 2008] |

|

|

Amended |

Improvements to NZ IFRSs [July 2010] |

|

|

Added |

NZ IFRS 9 (2009) [Nov 2009] |

|

|

Deleted |

NZ IFRS 9 (2010 [Nov 2010], NZ IFRS 9 (2013) [Dec 2013] and NZ IFRS 9 (2014) [Sept 2014] |

|

|

Added |

Improvements to NZ IFRSs [July 2010] |

|

|

Added |

NZ IFRS 9 (2010 [Nov 2010] |

|

|

Deleted |

NZ IFRS 9 (2013) [Dec 2013] and NZ IFRS 9 (2014) [Sept 2014] |

|

|

Added |

NZ IFRS 10 and NZ IFRS 11 [June 2011] |

|

|

Added |

NZ IFRS 13 [June 2011] |

|

|

Added |

Presentation of Items of |

|

|

Added |

Framework: Tier 1 and Tier 2 For-profit Entities [Nov 2012] |

|

|

Added |

NZ IFRS 9 (2013) [Dec 2013] |

|

|

Deleted |

NZ IFRS 9 (2014) [Sept 2014] |

|

|

Added |

NZ IFRS 9 (2014) [Sept 2014] |

|

|

Added |

NZ IFRS 16 [Feb 2016] |

|

|

Added |

Lack of Exchangeability [Nov 2023] |

|

|

Added |

Lack of Exchangeability [Nov 2023] |

|

|

Added |

Lack of Exchangeability [Nov 2023] |

|

|

Added |

Lack of Exchangeability [Nov 2023] |

|

|

Added |

Lack of Exchangeability [Nov 2023] |

|

|

Added |

Lack of Exchangeability RDR [Jan 2024] |

|

|

Added |

Lack of Exchangeability RDR [Jan 2024] |

|

|

Added |

Lack of Exchangeability RDR [Jan 2024] |

|

|

Added |

Lack of Exchangeability RDR [Jan 2024] |

|

|

Paragraphs A1 – A20 and preceding headings |

Added |

Lack of Exchangeability [Nov 2023] |

|

Amended |

Lack of Exchangeability RDR [Jan 2024] |

|

|

Amended |

Lack of Exchangeability RDR [Jan 2024] |

1Superseded by NZ IFRS 9 Financial Instruments (2014). NZ IFRS 9 (2014) restricted early application of earlier versions of NZ IFRS 9.

2Superseded by NZ IFRS 9 Financial Instruments (2014). NZ IFRS 9 (2014) restricted early application of earlier versions of NZ IFRS 9.