NZ AS 1 (Revised)

The Audit of Service Performance Information

Statement of Authority

NZ AS 1 (REVISED)

NEW ZEALAND AUDITING STANDARD 1 (REVISED) THE AUDIT OF SERVICE PERFORMANCE INFORMATION

Legal status of standard

This Standard was issued on 27 July 2023 by the New Zealand Auditing and Assurance Standards Board of the External Reporting Board (XRB) pursuant to section 12(b) of the Financial Reporting Act 2013.

This Standard is secondary legislation for the purposes of the Legislation Act 2019. An

In finalising this Standard, the New Zealand Auditing and Assurance Standards Board has carried out appropriate consultation in accordance with section 22(1) of the Financial Reporting Act 2013.

This Standard has been issued as a result of revising NZ AS 1 The Audit of Service Performance Information.

Copyright

© External Reporting Board (“XRB”) 2023

This XRB standard contains copyright material. Reproduction within New Zealand in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgment of the source.

Requests and enquiries concerning reproduction and rights for commercial purposes within New Zealand should be addressed to the Chief Executive, External Reporting Board at the following email address: enquiries@xrb.govt.nz

ISBN 978-1-99-100542-7

How to Read this Standard

New Zealand Auditing Standard (NZ AS) 1 (Revised), The Audit of Service Performance Information, should be read in conjunction with ISA (NZ) 200, Overall Objectives of the Independent

When standard takes effect (section 27 Financial Reporting Act 2013)

Accounting period in relation to which standards commence to apply (section 28 Financial Reporting Act 2013)

-

For an early adopter, those accounting periods following, and including, the early adoption accounting period:

-

For any other

auditor , those accounting periods following, and including, the first accounting period that begins on or after the mandatory date.

early adopter means an

early adoption accounting period means the accounting period

-

that begins before the mandatory date but has not ended or does not end before this standard takes effect (and to avoid doubt, that period may have begun before this standard takes effect); and

-

for which the early adopter

-

first applies this standard, and

-

discloses in its audit report for that accounting period that this standard has been applied for that period.

-

mandatory date means 1 January 2024.

Scope of the Standard

-

Assess whether each of the following aspects of the service performance information are appropriate and meaningful in accordance with the

applicable financial reporting framework : (Ref: Para. A3)- The elements/aspects of service performance that the entity has selected to report on.

-

The performance measures and/or descriptions the entity has used to report on what it has done in relation to those elements/aspects of service performance during the reporting period.

- The measurement basis or evaluation method used to measure or evaluate the performance measure and/or description.

- Assess whether the reported service performance information fairly reflects the actual service performance and is not materially misstated.

-

Misstatement – Misstatements can be intentional or unintentional, qualitative or quantitative, and include omissions. Misstatements can arise from error orfraud when:-

An element/aspect of service performance or performance measure and/or description, or a measurement basis or evaluation method is not appropriate and meaningful; or

-

An element/aspect of service performance or performance measure and/or description that would be appropriate and meaningful is omitted; or

-

Incorrectly measuring or evaluating the entity’s service performance.

-

-

Risk of Material – The risk that the service performance information is materially misstated prior to the audit. This consists of two components, described as follows at the assertion level:Misstatement -

Inherent risk – The susceptibility of an assertion about a performance measure and/or description, measurement basis or evaluation method or disclosure to amisstatement that could be material, either individually or when aggregated with other misstatements, before consideration of any relatedcontrols . -

Control risk – The risk that amisstatement that could occur in an assertion about a performance measure and/or description, measurement basis or evaluation method or disclosure and that could be material, either individually or when aggregated with other misstatements, will not be prevented, or detected and corrected, on a timely basis by the entity’s system of internalcontrols .

-

General Requirements

Conduct Engagement in Accordance with the ISAs (NZ)

Professional Judgement and Professional Scepticism

Documentation

-

Significant professional judgements made in audit procedures performed, the

audit evidence obtained, and conclusions reached. (Ref: Para. A8-A9) -

As far as possible, evidence of relevant relationships between the service performance information and the

financial statements .

Agreement on Audit Engagement Terms

-

The objective and scope of the audit. (Ref: Para. A12-A16)

-

The responsibilities of the

auditor with respect to the service performance information:-

To obtain an understanding of the process applied by the entity to select its elements/aspects of service performance, performance measures and/or descriptions and the measurement bases or evaluation methods.

-

To evaluate whether the selection of elements/aspects of service performance, performance measures and/or descriptions and measurement bases or evaluation methods present an appropriate and meaningful assessment of the entity’s service performance in accordance with the

applicable financial reporting framework . -

To evaluate whether the service performance information is prepared in accordance with the entity’s measurement bases or evaluation methods, in accordance with the

applicable financial reporting framework . -

To evaluate whether the overall presentation, structure and content of the service performance information represents the elements/aspects of service performance in accordance with the

applicable financial reporting framework .

-

-

The responsibilities of

those charged with governance , including that they acknowledge and understand their responsibility on behalf of the entity for:-

The selection of elements/aspects of service performance, performance measures and/or descriptions and measurement bases or evaluation methods that present service performance information that is appropriate and meaningful in accordance with the

applicable financial reporting framework . -

The preparation of service performance information in accordance with the entity’s measurement bases or evaluation methods, in accordance with the

applicable financial reporting framework . -

The overall presentation, structure and content of the service performance information in accordance with the

applicable financial reporting framework . -

Such internal control as

those charged with governance determine is necessary to enable the preparation of the service performance information that is free from materialmisstatement , whether due tofraud or error.

-

-

Reference to the expected form and content of the

auditor ’s report.

Obtaining an Understanding

Understanding the Entity

-

Why the entity exists and what it intends to achieve i.e., its purpose or objective.

-

What activities or services the entity performs.

-

Who the entity aims to serve i.e., the entity’s primary stakeholders and the primary users of the service performance report.

-

What is considered important to those stakeholders and users and what they may use the service performance information for.

Understanding Laws and Regulations

-

The legal and regulatory framework applicable to the entity and the industry or sector in which the entity operates, and laws and regulations that specify the form, content, preparation, publication, and audit of service performance information; and (Ref: Para. A18-A21)

-

How the entity is complying with that framework.

Understanding the Service Performance Information Reported

-

The

applicable financial reporting framework relevant to the service performance information. -

The process, including the rationale and logic the entity undertook to determine what elements/aspects of service performance, performance measures and/or descriptions and measurement bases or evaluation methods and judgements to report. (Ref: Para. A22- A24, A27)

-

The process the entity undertook to identify the intended users of the service performance information and the level of engagement with the intended users.

-

The measurement bases or evaluation methods used by the entity to assess the performance measures and/or descriptions and how these are made available to intended users. (Ref: Para. A79-A80)

-

Changes to the elements/aspects of service performance, performance measures and/or descriptions and the measurement bases or evaluation methods used to report its service performance compared to prior year, planned, forecast or prospective information. (Ref: Para. A25)

-

Where the entity intends to report its service performance information. (Ref: Para. A26)

Understanding the Components of the Entity’s System of Internal Control

Planning

-

Consider the factors that, in the

auditor ’sprofessional judgement , are significant in directing theengagement team ’s efforts in respect of the audit of service performance information. -

Determine the timing of when to evaluate whether the entity’s service performance information is appropriate and meaningful.

-

What elements/aspects of service performance and performance measures and/or descriptions the entity intends to report as part of its service performance information;

-

What measurement bases or evaluation methods the entity intends to use to measure or evaluate its performance; and

Compliance With the Applicable Financial Reporting Framework

Appropriate and Meaningful

-

It fairly reflects the

auditor ’s understanding of the entity’s performance from all other audit work performed on the audit. (Ref: Para. A36) -

It is likely to meet the needs of the intended user to enable an informed assessment of the entity’s service performance. (Ref: Para. A37-A38)

-

It relates to an element/aspect of service performance that significantly contributes to the entity’s core purpose, functions or objectives. (Ref: Para. A39)

-

There is likely to be sufficient appropriate evidence to support the performance measure and/or description.

-

It is capable of measurement or evaluation in a consistent manner from period to period. (Ref: Para. A40-A41)

-

It is presented in a way that is easy to follow, concise, logical and aggregated where appropriate so that it will enable a user to identify the main points of the entity’s service performance in that year.

Compliance With Laws and Regulations

Materiality

-

Nature, timing and extent of further audit procedures; and

-

The

auditor ’s tolerance formisstatement in relation to material service performance measures and/or descriptions.

-

The significant elements/aspects of service performance and related material performance measures and/or descriptions are appropriate and meaningful; and (Ref: Para. A51-A52)

-

The performance measures and/or descriptions, measurement bases or evaluation methods contain individual or collective misstatements, that based on the

auditor ’s judgement, are likely to influence the decisions of the intended users based on the information.

Identifying and Assessing Risks of Material Misstatement

-

At the service performance information level; and

-

At the assertion level for performance measures, descriptions or disclosures. (Ref: Para. A60-A62)

The Auditor’s Responses to Assessed Risks

-

Are responsive to assessed risks of material

misstatement at the assertion level; and -

Allow the

auditor to obtain sufficient appropriateaudit evidence regarding the assessed risks of materialmisstatement .

-

The

auditor ’s assessment of therisk of material includes the expectation thatmisstatement controls are operating effectively; or -

Where procedures other than tests of

controls cannot provide sufficient appropriateaudit evidence .

Audit Evidence

-

Elements/aspects of service performance, performance measures and/or descriptions, and measurement bases or evaluation methods are appropriate and meaningful; and

-

Performance measures and/or descriptions have been prepared in accordance with the entity’s measurement bases or evaluations methods; and

-

Performance measures and/or descriptions are not materially misstated.

Communicating with Those Charged with Governance

-

Any significant risks identified with the service performance information.

-

The

auditor ’s views about significant judgements made in reporting the entity’s service performance information, including any significant deficiencies or areas for improvement. (Ref: Para. A71) -

Significant difficulties, if any, encountered during the audit. (Ref: Para. A72)

-

Unless all of

those charged with governance are involved in managing the entity, significant matters arising during the audit that were discussed, or subject to correspondence withmanagement . (Ref: Para. A73) -

Matters involving non-compliance with laws and regulations with respect to service performance reporting obligations.

-

Deficiencies in internal control with respect to the service performance information that, in the

auditor ’sprofessional judgement , are of sufficient importance to merit attention.19 -

Uncorrected misstatements and the effect that they, individually or in aggregate, may have on the opinion on the service performance information in theauditor ’s report and request that they are corrected.20 -

Any modifications including the circumstances and the wording the

auditor expects to make to the opinion relating to service performance information in theauditor ’s report.21

Special Considerations: An Entity Using a Service Organisation, Groups and Using the Work of Another Practitioner

-

Where a

service organisation is used, obtain an understanding of the nature and significance of the services provided by theservice organisation and their effect on theuser entity ’s internal control relevant to the audit of service performance information sufficient to identify and assess the risks of materialmisstatement and design, and perform audit procedures responsive to those risks in accordance with ISA (NZ) 402.22 (Ref: Para. A74) -

Where the service performance information relates to a

group , obtain sufficient appropriateaudit evidence regarding the service performance information of the components and the aggregation or consolidation process in order to express an opinion on whether thegroup ’s service performance information is prepared, in all material respects, in accordance with theapplicable financial reporting framework . 23 (Ref: Para. A75) -

Where the service performance information includes information upon which another practitioner has expressed an opinion, communicate clearly with the other practitioner, when the

auditor intends to use the work of another practitioner about the scope and timing of the work and findings of the other practitioner, and evaluate the sufficiency and appropriateness of evidence obtained and the process for including related information in the service performance information. (Ref: Para. A76)

Using the Work of an Auditor’s Expert

Written Representations

-

The selection of elements/aspects of service performance, performance measures and/or descriptions and measurement bases or evaluation methods that present service performance information that is appropriate and meaningful in accordance with the

applicable financial reporting framework . -

The preparation of service performance information in accordance with the entity’s measurement bases or evaluation methods, in accordance with the

applicable financial reporting framework . -

The overall presentation, structure and content of the service performance information in accordance with the

applicable financial reporting framework . -

Such internal control as

those charged with governance determine is necessary to enable the preparation of the service performance information that is free from materialmisstatement , whether due tofraud or error.

Forming an Opinion

-

Whether sufficient, appropriate

audit evidence has been obtained; -

Whether

uncorrected misstatements are material, individually or collectively; and -

The

auditor ’s evaluation of whether the service performance information is prepared, in all material respects, in accordance with the entity’s measurement bases or evaluation methods, in accordance with theapplicable financial reporting framework .

-

The entity has presented service performance information that is appropriate and meaningful.

-

The measurement bases or evaluation methods are available to intended users. (Ref: Para. A79-A80)

-

When the information is prepared in accordance with a

fair presentation framework 27, the service performance information achieves fair presentation, including whether:-

The overall presentation of the service performance information has been undermined by including information that is not relevant or that obscures a proper understanding of the matters disclosed;

-

The overall presentation, structure and content of the service performance information represents the service performance of the entity in a manner that achieves fair presentation; and

-

The disclosure of the judgements made in reporting the service performance information, if applicable, is reasonable.

-

-

Any matters arising during the course of the audit of the

financial statements that may affect theauditor ’s evaluation of the service performance information. -

The impacts of any matters arising during the audit of the service performance information that may affect the

auditor ’s evaluation of thefinancial statements .

Report Content

-

Identify the service performance information;

-

State that the service performance information has been audited;

-

Identify the

applicable financial reporting framework ; and -

Refer to the measurement bases or evaluation methods (Ref: Para. A83)

-

State, in the basis for opinion section, that the audit of the service performance information was conducted in accordance with International Standards on Auditing (New Zealand) and New Zealand Auditing Standard 1 (Revised);

-

Describe the responsibilities of

those charged with governance for:-

The selection of elements/aspects of service performance, performance measures and/or descriptions and measurement bases or evaluation methods that present service performance information that is appropriate and meaningful in accordance with the

applicable financial reporting framework . -

The preparation of service performance information in accordance with the entity’s measurement bases or evaluation methods in accordance with the

applicable financial reporting framework . -

The overall presentation, structure and content of the service performance information in accordance with the

applicable financial reporting framework . -

Such internal control as

those charged with governance determine is necessary to enable the preparation of service performance information that is free from materialmisstatement , whether due tofraud or error.

When the financial report is prepared in accordance with afair presentation framework , the description of responsibilities shall refer to “the preparation and fair presentation of the service performance information” or the “preparation of service performance information that gives a true and fair view” as appropriate in the circumstances.28

-

-

In the “

auditor ’s responsibilities” section describe the audit of the service performance information by stating that, in accordance with the ISAs (NZ) and this New Zealand Auditing Standard, theauditor ’s responsibilities are to:-

Obtain an understanding of the process applied by the entity to select its elements/aspects of service performance, performance measures and/or descriptions and the measurement bases or evaluation methods.

-

Evaluate whether the selection of elements/aspects of service performance, performance measures and/or descriptions and measurement bases or evaluation methods present an appropriate and meaningful assessment of the entity’s service performance in accordance with the

applicable financial reporting framework . -

Evaluate whether the selected service performance information is prepared in accordance with the entity’s measurement bases or evaluation methods, in accordance with the

applicable financial reporting framework . -

Evaluate whether the overall presentation, structure and content of the service performance information represents the elements/aspects of service performance in accordance with the

applicable financial reporting framework , including where relevant its fair presentation.

-

Key Audit Matters

Modifications to the Opinion in the Independent Auditor’s Report

-

The

auditor concludes that either individually or collectively the elements/aspects of service performance, performance measure and/or descriptions, or measurement bases or evaluation methods are materially misstated in that it is not appropriate and meaningful and as such is not in accordance with theapplicable financial reporting framework , or -

The

auditor concludes, based on theaudit evidence obtained, that the service performance information is not individually or collectively free from materialmisstatement , or (Ref: Para. A86) -

The

auditor is unable to obtain sufficient appropriateaudit evidence to conclude that the service performance information, as a whole, is free from materialmisstatement .

Emphasis of Matter Paragraphs and Other Matter Paragraphs

Comparative Information

-

Prior period comparative service performance information agrees with disclosures presented in the prior period or when appropriate, have been restated; and

-

The elements/aspects of service performance, performance measure and/or descriptions, or measurement bases or evaluation methods is consistent with the current period or, if there have been changes, whether those changes have been properly accounted for and adequately presented and disclosed.

Prospective Service Performance Information

-

Assess whether the prospective service performance information agrees with the information presented in the published prospective service performance information: or

-

Assess that any changes have been clearly explained in the service performance information.

Other Information

-

The

other information and the service performance information; and -

The

other information and theauditor ’s knowledge obtained in the audit.

3ISA (NZ) 230, Audit Documentation, paragraphs 7-16

4 ISA (NZ) 210, Agreeing the Terms of Audit Engagements, paragraphs NZ9.1-NZ10.1

5 ISA (NZ) 315 (Revised 2019), Identifying and Assessing the Risks of Material Misstatement

6ISA (NZ) 300, Planning an Audit of Financial Statements, paragraph 7.

7PBE FRS 48, Service Performance Reporting, paragraph 7; Reporting Requirements for Tier 3 Public Sector Entities paragraphs A49-A50; Reporting Requirements for Tier 3 Not-for-Profit Entities, paragraphs A46-A47

8 ISA (NZ) 250 (Revised), Consideration of Laws and Regulations in an Audit of Financial Statements

9ISA (NZ) 320, Materiality in Planning and Performing an Audit, paragraph 11 and 14

10 ISA (NZ) 320, paragraph 5

11 ISA (NZ) 320, paragraphs 12 and 13

12 ISA (NZ) 315 (Revised 2019), paragraph 32

13 ISA (NZ) 330 The Auditor’s Responses to Assessed Risks

14 ISA (NZ) 330, paragraph 8

15 ISA (NZ) 330, paragraph 18

16ISA (NZ) 500, Audit Evidence, paragraph 6

17 ISA (NZ) 500 paragraph 8

18 ISA (NZ) 260 (Revised), Communication with Those Charged with Governance

19 ISA (NZ) 265, Communicating Deficiencies in Internal Control to Those Charged with Governance and Management

20 ISA (NZ) 450, Evaluation of Misstatements Identified during the Audit

21 ISA (NZ) 705 (Revised), Modifications to the Opinion in the Independent Auditor’s Report

22 ISA (NZ) 402, Considerations Relating to an Entity Using a Service Organisation

23 ISA (NZ) 600 (Revised), Special Considerations – Audit of Group Financial Statements (Including the Work of Component Auditors)

24 ISA (NZ) 620, Using the Work of an Auditor's Expert

25 ISA (NZ) 580, Written Representations

26 ISA (NZ) 700 (Revised), Forming an Opinion and Reporting on Financial Statements

27 When the service performance information is prepared in accordance with a

28 This is not required for tier 4 entities reporting under a

29 ISA (NZ) 701 Communicating Key Audit Matters in the Independent Auditor’s Report

Introduction (Ref: Para. 1)

Scope of the Standard (Ref: Para. 5)

Objective (Ref: Para. 7(a))

-

The elements/aspects of service performance that the entity has selected to report on. For example, provide safe drinking water to stakeholders.

-

The performance measures and/or descriptions the entity has used to report on what it has done in relation to the elements/aspects of service performance during the reporting period. For example, 100% of water supplied was safe.

-

The measurement basis or evaluation method used to measure or evaluate the performance measure and/or description. For example, Drinking Water Standards for New Zealand or internally generated safe drinking water criteria.

General Requirements (Ref: Para. 9, 11)

Conduct Engagement in Accordance with the ISAs (NZ)

Professional Judgement and Professional Scepticism

Documentation (Ref: Para. 12-13(a))

-

Planning: The overall engagement strategy, the engagement plan, capturing the nature of the plan, reflecting plans to make connections between the

financial statements and service performance information, any significant changes made during the engagement, and the reasons for the changes. -

Risks of material

misstatement : Key elements of theauditor ’s understanding in accordance with paragraphs 15-19; including the sources of information from which theauditor ’s understanding was obtained. -

Procedures: The nature, timing and extent of the further audit procedures performed, the linkage of those further audit procedures with the risks of material

misstatement , and the results of audit procedures. -

Evaluation of misstatements: Misstatements identified during the engagement and whether they have been corrected, the

auditor ’s conclusion as to whetheruncorrected misstatements are material, individually or collectively.

-

whether the service performance information is appropriate and meaningful (Ref: Para. 25).

-

the factors considered in determining materiality and what measures are material. (Ref: Para. 28)

Agreement on Audit Engagement Terms (Ref: Para. 14)

Scope

Obtaining an Understanding (Ref: Para. 15-19)

Understanding the Entity (Ref: Para. 15)

-

Enquires with

management andthose charged with governance ; -

Reading:

-

-

-

Founding documents such as rules, constitution or trust deed.

-

Statement of intent.

-

Past statements of service performance.

-

Funding documents or agreements.

-

Minutes from governance meetings.

-

Entity newsletters.

-

Entity’s public website.

-

Charities register.

-

Media reports.

-

-

Understanding Laws and Regulations (Ref: Para. 16)

Understanding the Service Performance Information Reported (Ref: Para. 17)

Forecast Service Performance Information

Understanding the Components of the Entity’s System of Internal Control (Ref: Para. 18)

Planning (Ref: Para. 20, 22)

Forecast Service Performance Information

Compliance With the Applicable Financial Reporting Framework (Ref: Para. 24)

-

For tier 1 and tier 2 public benefit entities, PBE FRS 48 Service Performance Reporting

-

For tier 3 public benefit entities:36

-

Reporting Requirements for Tier 3 Not-for-Profit Entities

-

Reporting Requirements for Tier 3 Public Sector Entities

-

-

For tier 4 public benefit entities:

-

Reporting Requirements for Tier 4 Not-for-Profit Entities

-

Reporting Requirements for Tier 4 Public Sector Entities Appropriate and Meaningful (Ref: Para. 25)

-

-

Whether the service performance information presents a neutral view including all significant aspects, both positive and negative.

-

Whether any service performance information is omitted, where this is an appropriate link to the service performance of the entity.

-

Whether there is potential for

management bias -

If the entity reports targets, how those targets may obscure a proper understanding of the entity’s service performance.

-

The results of surveys. For example, satisfaction surveys, or other evidence of stakeholder consultation, e.g., feedback, complaints which may indicate the appropriateness of the service performance information.

-

Whether the process to determine what service performance information to report involved the intended users and what information they may find helpful to assess the service performance of the entity - lowering the risk of

management bias -

External requirements or agreements with external parties that influence the entity’s service performance accountability.

-

Whether the service performance information was pre agreed with key stakeholders.

-

Guidelines developed and issued collectively by a

group or published in journals or results of benchmarking studies, for example, central agencies may provide guidance or establish requirements for the preparation of service performance information. Theauditor may need to evaluate the suitability of these guidelines to the entity’s circumstances and how these align to intended users’ needs. More detailed service performance reporting may be more appropriate. -

Whether an overly voluminous service performance report is detracting from the usefulness and relevance of the overall report.

-

Whether the service performance report is complete.

-

The service performance information shows clear and logical links between the element/aspect of service performance to be measured or evaluated and the entity’s overall purpose and strategies.

-

There is other potentially more relevant service performance information that could have been used and reasons why those were not included.

-

The entity has a clear understanding of its contribution toward longer term elements/aspects of service performance.

-

The entity uses a well-established performance framework, theory of change or intervention logic model to explain how its service performance during the reporting period relates to its broader aims and objectives or may have described predetermined objectives or specific performance goals or targets in agreements with key stakeholders, for example, a local authority’s Long-Term Plan, statement of intent, charter, recent plans and strategies or agreements with key funders. The selection of service performance information pre agreed with key stakeholders may have a lower risk of

management bias -

The service performance information reflects how the entity assesses its service performance for the purpose of internal decision making.

Forecast Service Performance Information

Materiality (Ref: Para. 27-31)

-

The importance of the element/aspect of service performance to achieving the entity’s service performance objectives. For example, whether the performance measure and/or description relates to the primary purpose of the entity. The more important the activity, the less tolerance for

misstatement . -

How the information is presented. For example, does the presentation draw attention to particular information? The

auditor may be less tolerant ofmisstatement in information that is given the most prominence. -

The extent of interest shown in particular aspects of service performance by, for example funders, key stakeholders or the public; and for example, whether the service performance information is likely to cause funders to increase or decrease funding in the entity. The higher the level of interest shown, the lower the tolerance for

misstatement . For matters where there is the most significant interest, theauditor may be less accepting of misleading or inaccurate information.

-

The economic, social, political and environmental effect of a project or an entity’s work, where there is a high level of wider societal interest in it, particularly high levels of public sensitivity, or relate to an activity that could be a

significant risk to the public. -

Whether a particular aspect of the service performance information is significant with regard to the nature, visibility and sensitivity of the information. For example, there has been a large number of complaints relating to it, or relates to an activity that is strongly linked to

management performance rewards. -

The relative volatility of reported service performance information. For example, if service performance information varies significantly from period to period.

-

The number of persons or entities affected.

-

Where there is information about achieving a target or threshold, and the relationship of the actual performance to the target. For example, the

auditor may be particularly diligent where a target has only just been achieved. -

Whether a

misstatement is material having regard to theauditor ’s understanding of known previous communications to users.

Misstatements

-

An element/aspect of service performance or performance measure or description, or a measurement basis or evaluation method selected is assessed by the

auditor as not being appropriate and meaningful; -

An element/aspect of service performance or performance measure and/or description is omitted that is assessed by the

auditor as being appropriate and meaningful; -

The information is not prepared in accordance with the entity’s measurement basis or evaluation method;

-

The entity’s service performance information is not in accordance with the

applicable financial reporting framework .

-

Misuse of language – that creates a misleading picture of the entity’s performance.

-

Misleading presentation – which highlights or downplays aspects of performance, to create a misleading picture of the entity’s service performance.

-

Bias – an emphasis is placed on good performance and downplays or omits poor performance i.e., isn’t neutral.

-

Omission of fact – something is left out that may be important to understanding the entity’s service performance or is important to intended users.

-

Incorrect measurement or evaluation – the service performance measure isn’t prepared in accordance with the measurement basis or evaluation method selected by the entity.

-

Where quantifiable service performance information misstates the level of actual performance beyond a determined level (the traditional application of materiality).

-

Misstatement of fact. -

Misrepresentation of trend – performance presented does not represent the facts available.

-

Unsubstantiated claims.

Identifying and Assessing Risks of Material Misstatement (Ref: Para. 32-33)

-

Occurrence – service performance that has been reported has occurred.

-

Attributable to the entity – the service performance reported by the entity includes only service performance that the entity has evidence to support its involvement with either directly or in conjunction with other entities with common goals.

-

Completeness – all important service performance that should have been reported has been included in the service performance information.

-

Accuracy – service performance has been reported, measured and described appropriately and is not inconsistent with the financial statement information.

-

Cut-off – service performance has been reported in the correct period.

-

Presentation – service performance is appropriately aggregated or disaggregated, clearly displayed and not misleading, and related disclosures are relevant and understandable.

-

Performance measures that use a measurement basis or evaluation method that may be subject to differing interpretations.

-

Performance measures that involve complexity in data collection and processing.

-

Performance measures that use a measurement basis or evaluation method that involves complex calculations.

-

Changes in the entity’s business that involve changes in service performance.

Audit Evidence (Ref: Para. 37-40)

-

Agreeing or reconciling amounts reported in the service performance information to any underlying financial and non-financial records.

-

Agreeing cross references between the service performance information and the

financial statements .

Communicating with Those Charged with Governance (Ref: Para. 41)

-

Extensive unexpected effort required to obtain sufficient appropriate

audit evidence . -

The unavailability of expected information.

Special Considerations: An Entity Using a Service Organisation, Groups and Using the Work of Another Practitioner (Ref: Para. 42)

-

A communication that the

auditor understands and complies with the requirements of Professional and Ethical Standard 137. -

The other practitioner’s professional competence.

-

The extent of the

engagement team ’s involvement in the work of the other practitioner.

ISA (NZ) 620 may also provide useful guidance with respect to using the work performed by another assurance practitioner.

Using the Work of an Auditor’s Expert (Ref: Para. 43)

-

The measurement of complex performance measures;

-

Assertions made about the entity’s performance, for example, when reporting on the impact that the entity had; -

Conformity assessments, ecolabelling and certification programmes.

Written Representations (Ref: Para. 44)

Forming an Opinion (Ref: Para. 17(d), 47(b))

-

Publicly, for example, readily available documents such as a published external assessment framework on a website.

-

Through inclusion in a clear manner in the presentation of the service performance information, in particular for entity-developed measurement bases or evaluation methods.

-

Through inclusion in a clear manner in the description of the performance measure and/or description itself, for example, number of meals delivered.

-

By general understanding, for example, the method of measuring time in hours and minutes. The

auditor may consider whether it is clear what the time is measuring. For example, an entity may measure its response time to an outage but will need to be clear as to whether the response time is measured from when a call is lodged, or measures the time taken to address a fault from when someone arrives to address the fault.

Report Content (Ref: Para. 49-51)

In our opinion, the accompanying [financial report/ performance report] presents fairly, in all material respects:

-

[the entity information as at December 31, 20X3;]

-

the financial position of the [entity] as at December 31, 20X3, and its financial performance, and its cashflows for the year then ended; and

-

the service performance for the year ended December 31, 20X3 in that the service performance information is appropriate and meaningful and prepared in accordance with the entity’s measurement bases or evaluation method

in accordance with [the

Key Audit Matters (Ref: Para. 52)

Modifications to the Opinion in the Independent Auditor’s Report (Ref: Para. 53-56)

-

The application of the measurement basis or evaluation method;

-

Inadequate disclosure of judgements made, where applicable; or

-

Incomplete disclosures that do not include all disclosures required by the

applicable financial reporting framework or do not achieve fair presentation of the service performance information.

Emphasis of Matter Paragraphs and Other Matter Paragraphs (Ref: Para. 57-58)

-

The underlying facts and information about the entity’s process to select what service performance to report on (e.g., the maturity of the entity’s process compared to others in the industry).

-

The source and method used to measure or evaluate the service performance information and whether they are externally established (e.g., established in legislation or externally established performance frameworks).

-

Any significant interpretations made in selecting the entity’s service performance information or applying the method(s) to measure or evaluate.

-

Whether there have been any changes in the service performance information disclosed or measurement bases or evaluation methods used.

-

Any other matters the

auditor considers necessary to assist intended users in making decisions based on the service performance information. -

Information the

auditor considers would enhance transparency and assist the user to understand the level of maturity that the entity has achieved in its reporting.

Other Information (Ref: Para. 61)

31 ISA (NZ) 240, The Auditors Responsibilities Relating to Fraud in an Audit of Financial Statements

32 ISA (NZ) 540 (Revised), Auditing Accounting Estimates and Related Disclosures

33 ISA (NZ) 550, Related Parties

34 ISA (NZ) 230, paragraph A9

35 ISA (NZ) 720 (Revised), The Auditor’s Responsibility Relating to Other Information

36Prior to periods beginning on or after 1 April 2024, the applicable financial reporting standards are PBE Simple Format Reporting – Accrual for tier 3 public benefit entities, and PBE Simple Format Reporting – Cash for tier 4 public benefit entities.

37 Professional and Ethical Standard 1, International Code of Ethics for Assurance Practitioners (including International Independence Standards) (New Zealand)

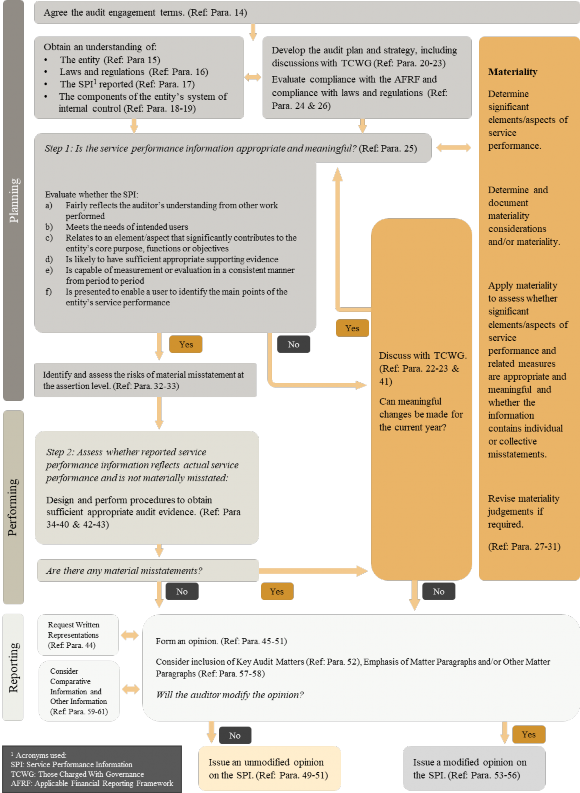

Flowchart of the Audit of Service Performance Information

This flowchart is to be read in conjunction with the standard, and is not intended to be exhaustive. The audit is an iterative process, and therefore the audit may not necessarily flow in the order presented below.

(Ref: Para. A11)

Illustrative Audit Engagement Letter including Service Performance Information38

The following is an example of an audit engagement letter for an audit of a [financial report/ performance report], which comprise

To [

[The objective and scope of the audit]

You have requested that we audit the [financial report/ performance report] of [ABC Entity (the “entity”)], which comprise the

The objectives of our audit are to obtain

[The responsibilities of the

We will conduct our audit of the

-

Identify and assess the risks of material

misstatement of the [financial report/ performance report], whether due tofraud or error, design and perform audit procedures responsive to those risks, and obtainaudit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a materialmisstatement resulting fromfraud is higher than for one resulting from error, asfraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control. -

Obtain an understanding of internal control relevant to the audit of the [financial report/ performance report] in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. However, we will communicate to you in writing concerning any significant deficiencies in internal control relevant to the audit of the [financial report/ performance report] that we have identified during the audit.

-

Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by [

management andThose Charged with Governance ]. -

Obtain an understanding of the process applied by the entity to select its elements/aspects of service performance, performance measures and/or descriptions and the measurement bases or evaluation methods.

-

Evaluate whether the selection of elements/aspects of service performance, performance measures and/or descriptions and measurement bases or evaluation methods present an appropriate and meaningful assessment of the entity’s service performance in accordance with [the

applicable financial reporting framework (e.g., PBE Standards)]. -

Evaluate whether the service performance information is prepared in accordance with the entity’s measurement bases or evaluation methods, in accordance with the

applicable financial reporting framework . -

Conclude on the appropriateness of the use of the going concern basis of accounting by [

Those Charged with Governance ] and, based on theaudit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the entity’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in ourauditor ’s report to the related disclosures in the [financial report/ performance report] or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on theaudit evidence obtained up to the date of ourauditor ’s report. However, future events or conditions may cause the entity to cease to continue as a going concern. -

Evaluate the overall presentation, structure and content of the [financial report/ performance report] and whether the [financial report/ performance report] represents the underlying transactions and events, and elements/aspects of service performance in accordance with the

applicable financial reporting framework in a manner that achieves fair presentation.

Because of the inherent limitations of an audit, together with the inherent limitations of internal control, there is an unavoidable risk that some material misstatements may not be detected, even though the audit is properly planned and performed in accordance with ISAs (NZ) and NZ AS 1 (Revised).

[The responsibilities of [

Our audit will be conducted on the basis that [

-

The preparation, and fair presentation of the [financial report/ performance report] in accordance with the

applicable financial reporting framework ; -

The selection of elements/aspects of service performance, performance measures and/or descriptions and measurement bases or evaluation methods that present service performance information that is appropriate and meaningful in accordance with the

applicable financial reporting framework ;

-

The preparation and fair presentation of service performance information in accordance with the entity’s measurement bases or evaluation methods, in accordance with the

applicable financial reporting framework ; -

The overall presentation, structure and content of the service performance information in accordance with the

applicable financial reporting framework ; -

Such internal control as [

Those Charged with Governance ] determine is necessary to enable the preparation of the [financial report/ performance report] that is free from materialmisstatement , whether due tofraud or error; and -

To provide us with:

-

Access to all information of which [

management and [Those Charged with Governance ]] are aware that is relevant to the preparation of the [financial report/ performance report] such as records, documentation and other matters; -

Additional information that we may request from [

management or [Those Charged with Governance ]] for the purpose of the audit; and -

Unrestricted access to persons within the entity from whom we determine it necessary to obtain

audit evidence .

As part of our audit process, we will request from [

We look forward to full cooperation from your team during our audit.

[Other relevant information]

[Insert other relevant information, such as fee arrangements, billings and other specific terms, as appropriate.]

[Reporting]

[Insert appropriate reference to the expected form and content of the

The form and content of our

Please sign and return the attached copy of this letter to indicate your acknowledgement of, and agreement with, the arrangements for our audit of the [financial report/ performance report] including our respective responsibilities.

[Signature in the name of the audit

Acknowledged and agreed on behalf of [

(signed)

Name and Title

Date

39 The addressees and references in the letter would be those appropriate in the circumstances of the engagement. It is important to refer to the appropriate persons – refer to ISA (NZ) 210 paragraph A22.

(Ref: Para. A78)

Illustrative Representation Letter including Service Performance Information40

The following illustrative letter includes written representations that are required by this standard and ISAs (NZ). It is assumed in this illustration that the

***

(Entity Letterhead)

(To

(Date)

This representation letter is provided in connection with your audit of the [financial report/ performance report] of [ABC Entity (the “entity”)] for the year ended December 31, 20X341 which comprise the

-

[the entity information as at December 31, 20X3; and]

-

the financial position of the entity as at December 31, 20X3, and its financial performance, and its cash flows for the year then ended; and

-

the service performance for the year ended December 31, 20X3 in that the service performance information is appropriate and meaningful and prepared in accordance with the entity’s measurement bases or evaluation methods

in accordance with [the

We confirm that (, to the best of our knowledge and belief, having made such enquiries as we considered necessary for the purpose of appropriately informing ourselves):

[Financial Report/ Performance Report]

-

We have fulfilled our responsibilities on behalf of the entity, as set out in the terms of the audit engagement dated [insert date], for:

-

-

The preparation, and fair presentation of the [financial report/ performance report] in accordance with the

applicable financial reporting framework -

The selection of elements/aspects of service performance, performance measures and/or descriptions and measurement bases or evaluation methods that present service performance information that is appropriate and meaningful in accordance with the

applicable financial reporting framework

-

The preparation of service performance information in accordance with the entity’s measurement bases or evaluation methods in accordance with the

applicable financial reporting framework ; -

The overall presentation structure and content of the service performance information in accordance with the

applicable financial reporting framework ; and -

Such internal control as we determine is necessary to enable the preparation of the [financial report/ performance report] that is free from material

misstatement , whether due tofraud or error. (NZ AS 1 (Revised))

-

-

The methods, the data and the significant assumptions used by us in making accounting estimates and their related disclosures are appropriate to achieve recognition, measurement or disclosure that is reasonable in the context of the

applicable financial reporting framework . (ISA (NZ) 540 (Revised)) -

Related party relationships and transactions have been appropriately accounted for and disclosed in thefinancial statements in accordance with theapplicable financial reporting framework . (ISA (NZ) 550) -

All events subsequent to the

date of the which require adjustment or disclosure have been adjusted or disclosed. (ISA (NZ) 56042)financial statements -

The effects of

uncorrected misstatements are immaterial, both individually and in the aggregate or collectively, to the [financial report/ performance report]. A list of theuncorrected misstatements is attached to the representation letter. (ISA (NZ) 450) -

[Any other matters that the

auditor may consider appropriate.]

Information Provided

-

We have provided you with43:

-

-

Access to all information of which we are aware that is relevant to the preparation of the [financial report/ performance report] such as records, documentation and other matters;

-

Additional information that you have requested from us for the purpose of the audit; and

-

Unrestricted access to persons within the entity from whom you determined it necessary to obtain

audit evidence .

-

-

All transactions have been recorded in the accounting records and are reflected in the

financial statements . -

We have disclosed to you the results of our assessment of the risk that the [financial report/ performance report] may be materially misstated as a result of

fraud . (ISA (NZ) 240) -

We have disclosed to you all information in relation to

fraud or suspectedfraud that we are aware of and that affects the entity and involves:

-

-

Management ; -

Employees who have significant roles in internal control; or

-

Others where the

fraud could have a material effect on the [financial report/ performance report]. (ISA (NZ) 240)

-

-

We have disclosed to you all information in relation to allegations of

fraud , or suspectedfraud , affecting the entity’s [financial report/ performance report] communicated by employees, former employees, analysts, regulators or others. (ISA (NZ) 240)

-

We have disclosed to you all known instances of non-compliance or suspected non-compliance with laws and regulations whose effects should be considered when preparing a [financial report/ performance report]. (ISA (NZ) 250)

-

We have disclosed to you the identity of the entity’s related parties and all the

related party relationships and transactions of which we are aware. (ISA (NZ) 550) -

We will provide the final version of the documents determined to comprise the

annual report to theauditor when available, and prior to its issuance by the entity.44 (ISA (NZ) 720 (Revised)) -

[Any other matters that the

auditor may consider necessary.]

Signed on behalf of [

|

...................... Name and Title |

...................... Name and Title |

41 Where the

42 ISA (NZ) 560, Subsequent events

43 If the

Illustrative

(Ref: Para. A81)

|

For purposes of this illustrative

|

INDEPENDENT

To [Appropriate Addressee]

Opinion

We have audited the [financial report/ performance report] of [ABC Entity (the “entity”)], which comprise the

In our opinion, the accompanying [financial report/ performance report] presents fairly, in all material respects, (or gives a true and fair view of):

-

[the entity information as at December 31, 20X3;]

-

the financial position of the entity as at December 31, 20X3, and its financial performance, and its cash flows for the year then ended; and

-

the service performance for the year ended December 31, 20X3 in that the service performance information is appropriate and meaningful and prepared in accordance with the entity’s measurement bases or evaluation methods

in accordance with [the

Basis for Opinion

We conducted our audit of the

Other than in our capacity as

[Reporting in accordance with the reporting requirements in ISA (NZ) 720 (Revised) – see Illustration 1 in Appendix 2 of ISA (NZ) 720 (Revised).]

Responsibilities of [

[

-

The preparation, and fair presentation of the [financial report/ performance report] in accordance with the

applicable financial reporting framework ; -

The selection of elements/aspects of service performance, performance measures and/or descriptions and measurement bases or evaluation methods that present service performance information that is appropriate and meaningful in accordance with the

applicable financial reporting framework ; -

The preparation and fair presentation of service performance information in accordance with the entity’s measurement bases or evaluation methods, in accordance with the

applicable financial reporting framework ; -

The overall presentation, structure and content of the service performance information in accordance with the

applicable financial reporting framework ; and -

Such internal control as [

Those Charged with Governance ] determine is necessary to enable the preparation of a [financial report/ performance report] that is free from materialmisstatement , whether due tofraud or error.

In preparing the [financial report/ performance report], [

Our objectives are to obtain

A further description of the

|

Paragraph 41(b) of ISA (NZ) 700 (Revised) explains that the shaded material below can be located in an Appendix to the Paragraph 41(c) of ISA (NZ) 700 (Revised) explains that when law, regulation or ISAs (NZ) expressly permit, reference can be made to a website of an appropriate authority that contains the description of the As part of an audit in accordance with ISAs (NZ) and NZ AS 1 (Revised), we exercise

We communicate with [ |

[Signature in the name of the audit

[

[Date]

(Ref: Para. A87)

Illustrations of

-

Illustration 1: An

auditor ’s report containing anunmodified opinion on thefinancial statements and a qualified opinion due to a materialmisstatement of the service performance information. -

Illustration 2: An

auditor ’s report containing anunmodified opinion on thefinancial statements and a qualified opinion due to theauditor ’s inability to obtain sufficient appropriateaudit evidence about a single element of the service performance information. -

Illustration 3: An

auditor ’s report containing a qualified opinion on both thefinancial statements and the service performance information due to theauditor ’s inability to obtain sufficient appropriateaudit evidence about a single element of thefinancial statements . -

Illustration 4: An

auditor ’s report containing anunmodified opinion on thefinancial statements and an adverse opinion on the service performance information due to the service performance information being materially misstated.

|

For purposes of these illustrative

|

Illustration 1: An

INDEPENDENT

To [Appropriate Addressee]

Opinions

We have audited the [financial report/ performance report] of [ABC Entity (the “entity”)], which comprise the

Opinion on the

In our opinion, the accompanying [financial report/ performance report] presents fairly, in all material respects, (or gives a true and fair view of):

-

[the entity information as at December 31, 20X3; and]

-

the financial position of the entity as at December 31, 20X3, and its financial performance, and its cash flows for the year then ended;

in accordance with [the

Qualified Opinion on the Service Performance Information

In our opinion, except for the effects of the matter described in the Basis for Qualified Opinion on the Service Performance Information section of our report, the accompanying [financial report/ performance report] presents fairly, in all material respects, (or gives a true and fair view of) the service performance for the year ended December 31, 20X3 in that the service performance information is appropriate and meaningful and prepared accordance with the entity’s measurement bases or evaluation methods in accordance with [the

Basis for Opinions, Including Basis for Qualified Opinion on the Service Performance Information

[As reported in the service performance information on page xx, the entity has identified its service performance as [describe improvements reported or description of the difference that the entity has made] and measured this performance by [list performance measures and/or descriptions reported] to report its service performance. The entity has not been able to provide evidence of its role in those particular improvements and therefore should not have reported this improvement.]

We conducted our audit of the

Other than in our capacity as

[Reporting in accordance with the reporting requirements in ISA (NZ) 720 (Revised) – see Illustration 6 in Appendix 2 of ISA (NZ) 720 (Revised). The last paragraph of the

Responsibilities of [

[Reporting in accordance with NZ AS 1 (Revised) – see Appendix 4].

[Reporting in accordance with NZ AS 1 (Revised) – see Appendix 4].

[Signature in the name of the audit

[

[Date]

Illustration 2: An

INDEPENDENT

To [Appropriate Addressee]

Opinions

We have audited the [financial report/ performance report] of [ABC Entity (the “entity”)], which comprise the

Opinion on the

In our opinion, the accompanying [financial report/ performance report] presents fairly, in all material respects, (or gives a true and fair view of):

-

[the entity information as at December 31, 20X3; and]

-

the financial position of the entity as at December 31, 20X3, and its financial performance, and its cash flows for the year then ended

in accordance with [the

Qualified Opinion on the Service Performance Information

In our opinion, except for the effects of the matter described in the Basis for Qualified Opinion on the Service Performance Information section of our report, the accompanying [financial report/ performance report] presents fairly, in all material respects, (or gives a true and fair view of) the service performance for the year ended December 31, 20X3 in that the service performance information is appropriate and meaningful and prepared in accordance with the entity’s measurement bases or evaluation methods in accordance with [the

Basis for Opinions, Including Basis for Qualified Opinion on the Service Performance Information

[Some significant performance measures of the entity, rely on information from third parties, such as (give examples). The entity’s control over much of this information is limited, and there are no practical audit procedures to determine the effect of this limited control. For example, [describe performance measure and explain where information comes from that we are unable to independently test.]]

We conducted our audit of the

Other than in our capacity as

[Reporting in accordance with the reporting requirements in ISA (NZ) 720 (Revised) – see Illustration 6 in Appendix 2 of ISA (NZ) 720 (Revised). The last paragraph of the

Responsibilities of [

[Reporting in accordance with NZ AS 1 (Revised) – see Appendix 4].

[Reporting in accordance with NZ AS 1 (Revised) – see Appendix 4].

[Signature in the name of the audit

[

[Date]

Illustration 3: An

INDEPENDENT

To [Appropriate Addressee]

Qualified Opinion

We have audited the [financial report/ performance report] of [ABC Entity (the “entity”)], which comprise the

In our opinion, except for the effects of the matter described in the Basis for Qualified Opinion section of our report, the accompanying [financial report/ performance report] presents fairly, in all material respects (or gives a true and fair view of):

-

[the entity information as at December 31, 20X3; and]

-

the financial position of the entity as at December 31, 20X3, and its financial performance, and its cash flows for the year then ended; and

-

the service performance for the year ended December 31, 20X3 in that the service performance information is appropriate and meaningful and prepared in accordance with the entity’s measurement bases or evaluation methods

in accordance with [the

Basis for Qualified Opinion

[As outlined on page xx of the [financial report/ performance report], entity has not applied the requirements of the

We conducted our audit of the

Other than in our capacity as

[Reporting in accordance with the reporting requirements in ISA (NZ) 720 (Revised) – see Illustration 6 in Appendix 2 of ISA (NZ) 720 (Revised). The last paragraph of the

Responsibilities of [

[Reporting in accordance with NZ AS 1 (Revised) – see Appendix 4].

[Reporting in accordance with NZ AS 1 (Revised) – see Appendix 4].

[Signature in the name of the audit

[

[Date]

Illustration 4: An

INDEPENDENT

To [Appropriate Addressee]

Opinions

We have audited the [financial report/ performance report] of [ABC Entity (the “entity”)], which comprise the

Opinion on the

In our opinion, the accompanying [financial report/ performance report] presents fairly, in all material respects, (or gives a true and fair view of):

-

[the entity information as at December 31, 20X3; and]

-

the financial position of the entity as at December 31, 20X3, and its financial performance, and its cash flows for the year then ended

in accordance with [the

Adverse Opinion on the Service Performance Information

In our opinion, because of the significance of the matter discussed in the Basis for Adverse Opinion on the Service Performance Information section of our report, the accompanying [financial report/ performance report] does not present fairly (or does not give a true and fair view of) the service performance information on pages x to xx for the year ended December 31, 20X3 that is appropriate and meaningful and prepared in accordance with the entity’s measurement bases or evaluation methods and in accordance with [the

Basis for Adverse Opinion on the Service Performance Information

[As reported in the service performance information on page xx, the entity has identified its service performance to include [describe improvements reported or description of the difference that the entity has made] and measured this performance by [describe performance measures and/or descriptions reported] to report its service performance. We do not consider that these performance measures will enable an appropriate and meaningful assessment of the service performance of the entity for the year ended December 31, 20X1 to be made. Had the entity presented more appropriate and meaningful performance measures, the service performance information would have been materially affected. The effects on the service performance information, reporting performance measures and/or descriptions including xxx and linking to its responsibility for yyyy.]

We conducted our audit of the

Other than in our capacity as

[Reporting in accordance with the reporting requirements in ISA (NZ) 720 (Revised) – see Illustration 7 in Appendix 2 of ISA (NZ) 720 (Revised). The last paragraph of the

Responsibilities of [

[Reporting in accordance with NZ AS 1 (Revised) – see Appendix 4].

[Reporting in accordance with NZ AS 1 (Revised) – see Appendix 4].

[Signature in the name of the audit

[

[Date]

A. CONFORMING AMENDMENTS TO XRB Au1 APPLICATION OF AUDITING AND ASSURANCE STANDARDS

…

Appendix 2A

This appendix lists the New Zealand Auditing Standards to be applied in conjunction with the International Standards on Auditing (New Zealand) in conducting an audit of general purpose financial reports which comprise the

NZ AS 1 (Revised) The Audit of Service Performance Information

…

B. CONFORMING AMENDMENTS TO AUDITING STANDARDS AS A RESULT OF THE REVISIONS TO PBE FINANCIAL REPORTING STANDARDS

Revisions to the titles of the Tier 3 and Tier 4 PBE Financial Reporting Standards requires conforming amendments wherever the title appears including in the following standards:

-

ISA (NZ) 200, Overall Objectives of the Independent

Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing (New Zealand) -

ISA (NZ) 210, Agreeing the Terms of Audit Engagements

-

ISA (NZ) 700 (Revised), Forming an Opinion and Reporting on

Financial Statements

Revisions are as follows:

-

Public Benefit Entity Simple Format Reporting – Accrual (Public Sector) (PBE SFR – A (PS));

-

Public Benefit Entity Simple Format Reporting – Accrual (Not-For-Profit) (PBE SFR – A (NFP)).

-

Public Benefit Entity Simple Format Reporting – Cash (Public Sector);

-

Public Benefit Entity Simple Format Reporting – Cash (Not-For-Profit).

-

Reporting Requirements for Tier 3 Public Sector Entities (Tier 3 (PS) Standard);

-

Reporting Requirements for Tier 3 Not-for-Profit Entities (Tier 3 (NFP) Standard).

-

Reporting Requirements for Tier 4 Public Sector Entities (Tier 4 (PS) Standard);

-

Reporting Requirements for Tier 4 Not-for-Profit Entities (Tier 4 (NFP) Standard).

C. CONFORMING AMENDMENT TO ILLUSTRATIVE AUDIT REPORTS

Wherever an illustrative audit report refers to the

A further description of the

D. CONSEQUENTIAL AMENDMENT TO NZ AS 1 THE AUDIT OF SERVICE PERFORMANCE INFORMATION

This standard amends the commencement and application date of NZ AS 1 The Audit of Service Performance Information. Underline and strikethrough are used to indicate changes.

…

Effective DateCommencement and application

5. This NZ AS is effective for audits of service performance information included in the general purpose financial report for periods beginning on or after 1 January 2023. Early adoption is permitted.

The accounting periods in relation to which this standard commences to apply are:

-

For an early adopter, those accounting periods following, and including, the early adoption accounting period:

-

For any other

auditor , those accounting periods following, and including, the first accounting period that begins on or after the mandatory date.

early adopter means an

early adoption accounting period means the accounting period:

-

that begins before the mandatory date but has not ended or does not end before this standard takes effect (and to avoid doubt, that period may have begun before this standard takes effect); and

-

for which the early adopter first applies this standard.

mandatory date means 1 January 2024.