Statement of Authority

Financial Reporting Standard No. 44 New Zealand Additional Disclosures (FRS-44)

Issued April 2011 and incorporates amendments to 31 December 2023

This Standard was issued by the New Zealand Accounting Standards Board of the External Reporting Board pursuant to section 24(1)(a) of the Financial Reporting Act 1993.

This Standard is a Regulation for the purposes of the Regulations (Disallowance) Act 1989.

Reporting entities that are subject to this Standard are required to apply the Standard in accordance with the commencement and application provisions set out in paragraphs 13 to 26.

Copyright

© External Reporting Board (XRB) 2011

This XRB Standard contains copyright material.

Reproduction in unaltered form (retaining this notice) is permitted for personal and non-commercial use subject to the inclusion of an acknowledgement of the source.

Requests and enquiries concerning reproduction and rights for commercial purposes within New Zealand should be addressed to the Chief Executive, External Reporting Board at the following email address: enquiries@xrb.govt.nz

ISBN 978-1-927174-54-8

How to Read this Standard

Financial Reporting Standard No. 44 New Zealand Additional Disclosures (FRS-44) is set out in paragraphs 1–26. All the paragraphs have equal authority. Definitions of terms are given in the Glossary.

FRS-44 should be read in the context of its objective and the New Zealand Equivalent to the IASB Conceptual Framework for Financial Reporting. NZ IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors provides a basis for selecting and applying accounting policies in the absence of explicit guidance.

Compliance with NZ IFRS

*5 An entity whose financial statements comply with New Zealand equivalents to International Financial Reporting Standards (NZ IFRS) shall make an explicit and unreserved statement of such compliance in the notes. An entity shall not describe financial statements as complying with NZ IFRS unless they comply with all the requirements of NZ IFRS.

RDR5.1 A Tier 2 entity whose financial statements comply with New Zealand equivalents to International Financial Reporting Standards Reduced Disclosure Regime (NZ IFRS RDR) shall make an explicit and unreserved statement of such compliance in the notes. An entity shall not describe financial statements as complying with NZ IFRS RDR unless they comply with all the requirements of NZ IFRS RDR.

IFRS issued but not yet effective

*6.1 When an IFRS has been issued by the International Accounting Standards Board but the equivalent NZ IFRS has yet to be issued by the XRB, an entity must disclose the information specified in paragraphs 30 and 31 of NZ IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors in relation to that IFRS.

Reporting framework

7 An entity shall disclose in the notes:

-

the statutory basis or other reporting framework, if any, under which the financial statements have been prepared;

-

a statement whether the financial statements have been prepared in accordance with GAAP; and

-

that, for the purposes of complying with GAAP, it is a for-profit entity.

RDR7.1 If an entity elects to report in accordance with NZ IFRS RDR, it shall disclose in the notes the criteria that establish the entity as eligible to report in accordance with NZ IFRS RDR.

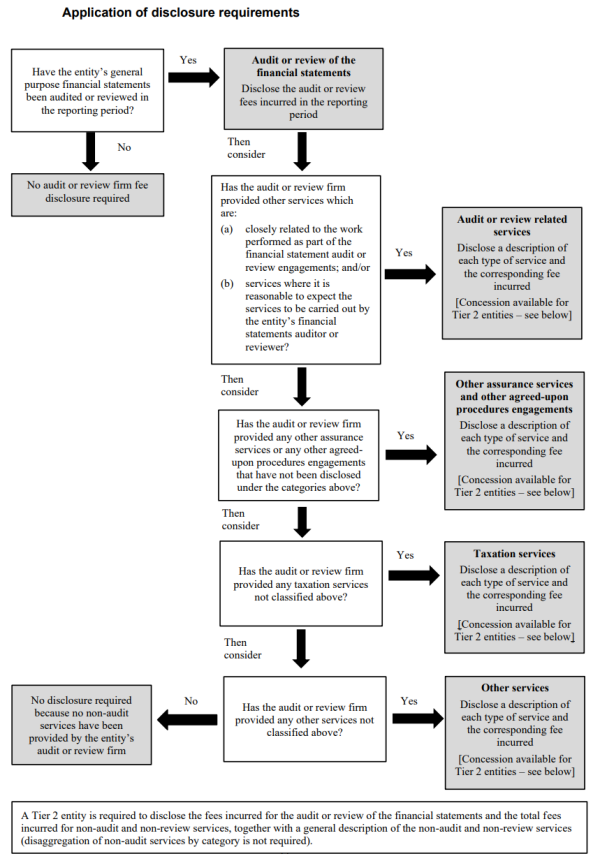

Fees for audit firms’ services

8.1 Paragraph 8.3 requires an entity to disclose information about the fees incurred in the reporting period for:

-

the audit or review of the entity’s financial statements; and

-

each other type of service provided by the entity’s audit or review firm.

8.2 The objective of this disclosure is to provide information that will assist users of general purpose financial statements to assess the extent to which non-audit services1 have been provided by the entity’s audit or review firm in the reporting period.

8.3 An entity shall disclose the fees incurred for services received from each audit or review firm2, separately for:

- the audit or review of the financial statements (see paragraphs 8.9 – 8.15);

- * each type of other service performed by the entity’s audit or review firm during the reporting period, using the following categories:

-

audit or review related services (see paragraphs 8.17 – 8.22);

-

other assurance services and other agreed-upon procedures engagements (see paragraphs 8.23 – 8.27);

-

taxation services (see paragraphs 8.28 – 8.30); and

-

other services (see paragraphs 8.32 – 8.34).

RDR8.3 A Tier 2 entity shall disclose the total fees incurred for services other than the audit or review of the financial statements provided by the entity’s audit or review firm, and a general description of these services.

8.4 Paragraph 8.3 requires the separate disclosure (under specified categories) of the fees incurred for services received from:

-

the entity’s audit or review firm; and

-

each other audit or review firm involved in any element of the audit or review of the entity’s financial statements, including the subsidiary financial statements when consolidated financial statements are presented.

8.5 The disclosure of the fees ‘incurred’ for services received from each audit or review firm, as required by paragraph 8.3 and paragraph RDR 8.3, will be based on the amount of fees expensed (and/or capitalised) by the entity during the reporting period. The fee will include any disbursements incurred in connection with providing the services (such as travel and accommodation costs).

8.6 The disclosure of fees incurred for fees covered by paragraph 8.3(b) and paragraph RDR 8.3, is required only when the audit or review firm has performed (or is performing) a financial statement audit or review engagement.

8.7 The descriptions used in this Standard for an ‘audit engagement’, a ‘review engagement’, an ‘agreed-upon procedures engagement’ and an ‘assurance engagement’, are based on the definitions of these terms as used in the professional and ethical standards and other standards issued by the New Zealand Auditing and Assurance Standards Board (NZAuASB).

8.8 When an entity incurs a single fee for a bundle of services from its audit or review firm, the entity shall, when practical, allocate the fee to each different type of service, to meet the disclosure objective in paragraph 8.2.

Audit or review of the financial statements

8.9 Fees for the audit or review of the financial statements refer to the audit or review of the entity’s general purpose financial statements, as presented in accordance with NZ IAS 1 Presentation of Financial Statements or NZ IAS 34 Interim Financial Reporting.

8.10 A financial statement audit engagement is a reasonable assurance engagement where an assurance practitioner expresses an opinion on whether the historical financial statements are prepared, in all material respects, in accordance with an applicable financial reporting framework. A financial statement audit engagement is conducted in accordance with applicable auditing and assurance standards.

8.11 A financial statement review engagement is a limited assurance engagement where an assurance practitioner provides a conclusion as to whether anything has come to their attention to indicate that the historical financial statements have not been prepared, in all material respects, in accordance with an applicable financial reporting framework. A financial statement review engagement is conducted in accordance with applicable auditing and assurance standards.

8.12 The total fees for the audit or review of the financial statements include all the services performed by the auditor as required to enable them to issue an audit opinion or review conclusion on the financial statements and provide other required communications to those charged with governance as part of the audit or review engagement.

8.13 The total fees under this category include work performed in relation to the:

-

annual financial statement audit or review engagement; and

-

interim financial statement audit or review engagement (if applicable).

8.14 The total fees under this category also include, when consolidated financial statements are presented, any fees incurred for the audit or review of the entity’s subsidiaries' financial information. The total fees disclosed under this category will include any additional fees incurred as a result of issuing an audit opinion or review conclusion on the financial statements of the subsidiary entities.

8.15 Examples of services that form part of the financial statement audit or review engagement include the following.

-

Attendance at audit committee meetings, board meetings, or annual general meetings for the purpose of discussing matters arising as a result of the financial statement audit or review engagement.

-

Discussions with management about audit or accounting matters that arise during or as a result of the financial statement audit or review engagement.

-

Preparation of a “management letter” to those charged with governance to report on the outcomes of the financial statement audit or review engagement, including advice and recommendations to improve the internal control environment.

-

Time incurred in connection with the audit or review of the income tax accrual or deferred tax balances as reported in the financial statements.

Audit or review related services

*8.17 Fees for audit or review related services include services which are:

-

closely related to the work performed as part of the financial statement audit or review engagement, but which are not required to complete the audit or review engagement described in paragraphs 8.9 – 8.15; and/or

-

services where it is reasonable to expect the services to be carried out by the entity’s financial statements auditor or reviewer.

*8.17A Services classified in this category may include assurance services or other types of services, such as agreed- upon procedures engagements, provided that the nature of the services is consistent with paragraph 8.17.

*8.18 Services that meet the description of audit or review related services in paragraph 8.17 include those services that are largely carried out by members of the financial statement audit or review engagement team, and this work generally relies on synergies in knowledge gained from undertaking the financial statement audit or review engagement.

*8.19 Audit or review related services also include services which are required by legislation or regulation to be performed by a suitably qualified auditor or assurance practitioner, when such services meet the description in paragraph 8.17.3

*8.20 To satisfy the disclosure requirements in paragraph 8.3(b)(i), the entity shall:

-

describe the nature of each type of audit or review related service; and

-

disclose the total fees for each type of audit or review related service.

*8.20A In disclosing the information required in paragraph 8.20, an entity shall categorise each type of audit or review related service as follows:

-

assurance engagements;

-

agreed-upon procedures engagements; or

-

other non-assurance engagements.

*8.21 Examples of types of audit or review related services could include:

-

engagements concerning summary financial statements and/or forecast financial statements;

-

reporting on whether processes, procedures, and controls relating to the financial reporting system are suitably designed and operating effectively;4

-

assurance engagements on solvency returns for insurance entities; and

-

agreed-upon procedures engagements that meet the description in paragraph 8.17 (see paragraphs 8.22A and 8.22B) – examples of such agreed-upon procedures engagements could include reporting on banking covenant calculations and reporting on the use of grant funding.

*8.22 Audit or review related services will also include any fees incurred by the reporting entity that arise from the audit or review of the entity’s associates, joint ventures, and/or other related entity financial statements.5

*8.22A An agreed-upon procedures engagement involves a practitioner performing procedures that have been agreed-upon by the practitioner and the engaging party, where the engaging party has acknowledged that the procedures performed are appropriate for the purpose of the engagement. The practitioner communicates the agreed-upon procedures performed and the related findings in the agreed-upon procedures report. The engaging party and other intended users consider for themselves the agreed-upon procedures and findings reported by the practitioner and draw their own conclusions from the work performed by the practitioner. An agreed-upon procedures engagement is not an audit, review or other assurance engagement. An agreed-upon procedures engagement does not involve obtaining evidence for the purpose of the practitioner expressing an opinion or an assurance conclusion in any form. Agreed-upon procedures engagements are carried out in accordance with applicable professional standards, including relevant ethical requirements.6

*8.22B Agreed-upon procedures engagements shall be classified as either audit or review related services, or as other assurance services and other agreed-upon procedures engagements, based on the nature of the engagement and the application of the category descriptions. Judgement may be required in making this assessment.

Other assurance services and other agreed-upon procedures engagements

*8.23 Other assurance services and other agreed-upon procedures engagements include:

-

any assurance services provided by an audit or review firm which have not been classified under the categories listed in paragraphs 8.3(a) or 8.3(b)(i); and

-

any agreed-upon procedures engagements provided by an audit or review firm which have not been classified under the category in paragraph 8.3(b)(i).

*8.24 An assurance service involves an independent assurance practitioner evaluating information against certain criteria and expressing a conclusion about the information as a result of this evaluation, with a view to enhance the confidence of the intended users of this conclusion. Assurance engagements are conducted in accordance with applicable assurance standards.

*8.24A An agreed-upon procedures engagement is described in paragraph 8.22A.

*8.25 This category includes assurance services and agreed-upon procedures engagements that do not rely significantly on synergies in knowledge gained from undertaking the financial statement audit or review engagement.

*8.26 To satisfy the disclosure requirements in paragraph 8.3(b)(ii), the entity shall:

-

describe the nature of each type of other assurance service and other agreed-upon procedures engagement; and

-

disclose the total fees for each type of other assurance service and other agreed-upon procedures engagement.

*8.26A In disclosing the information required in paragraph 8.26, an entity shall categorise each type of service as follows:

-

assurance engagements; or

-

agreed-upon procedures engagements.

*8.27 Examples of types of other assurance services and other agreed-upon procedures engagements could include:

-

assurance engagements on greenhouse gas statements or other sustainability reports that are not part of the financial statements;

-

assurance engagements on adherence to cyber/cloud security procedures;

-

other regulatory assurance engagements which are not considered to be audit or review related services; and

-

those agreed-upon procedures engagements that are not considered to be audit or review related services – an example of such agreed-upon procedures engagements could be reporting on health and safety.

Taxation services

*8.28 Taxation services comprise non-audit and non-assurance services relating to ascertaining the entity’s tax liabilities (or entitlements) or satisfying other obligations under taxation law. This category excludes the review of tax balances or disclosures as part of performing the audit or review of the general purpose financial statements.

*8.29 To satisfy the disclosure requirements in paragraph 8.3(b)(iii), the entity shall:

-

describe the nature of each type of taxation service; and

-

disclose the total fees for each type of taxation service.

*8.30 Examples of types of taxation services include:7

-

tax return preparation;

-

tax calculations to prepare accounting entries;

-

transfer pricing services;

-

tax planning and other tax advisory services;

-

tax services involving valuations; and

-

assistance in the resolution of tax disputes.

Other services

*8.32 Other services include any other services provided by the audit or review firm other than the services classified under the categories listed in paragraphs 8.3(a) and 8.3(b)(i) –(iii).

*8.33 To satisfy the disclosure requirements in paragraph 8.3(b)(iv), the entity shall:

-

describe the nature of each type of other service; and

-

disclose the total fees for each type of other service.

*8.34 Examples of types of other services include:8

-

accounting and bookkeeping;

-

administration;

-

valuations (including actuarial valuations);

-

internal audit;

-

information technology (including financial information systems);

-

litigation support;

-

legal;

-

recruitment and remuneration;

-

corporate finance and restructuring; and

-

business acquisition due diligence.

8.36 The flowchart below illustrates the application of the disclosure requirements concerning fees incurred for services provided by audit or review firms.

Imputation credits

*9.1 The term ‘imputation credits’ is used in paragraphs 9.2 and 9.4 to also mean ‘franking credits’. The disclosures required by paragraphs 9.2 and 9.4 shall be made separately in respect of any New Zealand imputation credits and any Australian imputation credits.

*9.2 An entity shall disclose the amount of imputation credits available for use in subsequent reporting periods.

*9.3 For the purposes of determining the amount required to be disclosed in accordance with paragraph 9.2, entities may have:

-

imputation credits that will arise from the payment of the amount of the provision for income tax;

-

imputation debits that will arise from the payment of dividends recognised as a liability at the reporting date; and

-

imputation credits that will arise from the receipt of dividends recognised as receivables at the reporting date.

*9.4 Where there are different classes of investors with different entitlements to imputation credits, disclosures shall be made about the nature of those entitlements for each class where this is relevant to an understanding of them.

Reconciliation of net operating cash flow to profit (loss)

*10 When an entity uses the direct method to present its statement of cash flows, the financial statements shall provide a reconciliation of the net cash flow from operating activities to profit (loss).

Prospective financial statements

11.1 Where an entity has published general purpose prospective financial statements for the period of the financial statements, the entity shall present a comparison of the prospective financial statements with the historical financial statements being reported. Explanations for major variations shall be given.

11.2 Financial Reporting Standard No. 42 Prospective Financial Statements defines general purpose prospective financial statements. Legislative or other requirements may require a comparison with originally published information, the most recently published information, or both.

12.1–12.10 [Deleted by NZASB]

Going concern disclosures

12A.1 When preparing financial statements, paragraph 25 of NZ IAS 1 Presentation of Financial Statements requires management to make an assessment of an entity’s ability to continue as a going concern. It requires an entity to prepare financial statements on a going concern basis unless management either intends to liquidate the entity or to cease trading, or has no realistic alternative but to do so. Furthermore, when management is aware, in making its assessment, of material uncertainties related to events or conditions that may cast significant doubt upon the entity’s ability to continue as a going concern, paragraph 25 of NZ IAS 1 requires disclosure of those uncertainties. When such material uncertainties exist, to the extent not already disclosed in accordance with paragraph 25 of NZ IAS 1, an entity that prepares its financial statements on a going concern basis shall disclose:

-

That there are one or more material uncertainties related to events or conditions that may cast significant doubt on the entity’s ability to continue as a going concern;

-

Information about the principal events or conditions giving rise to those material uncertainties;

-

Information about management’s plans to mitigate the effect of those events or conditions; and

-

That, as a result of those material uncertainties, it may be unable to realise its assets and discharge its liabilities in the normal course of business.

12A.2 Paragraph 122 of NZ IAS 1 requires an entity to disclose the judgements, apart from those involving estimations (see

paragraph 125 of NZ IAS 1), that management has made in the process of applying the entity’s accounting policies that have the most significant effect on the amounts recognised in the financial statements.

Paragraph 125 of NZ IAS 1 requires an entity to disclose information about the assumptions it makes about the future, and other major sources of estimation uncertainty at the end of the reporting period, that have a significant risk of resulting in a material adjustment to the carrying amounts of assets and liabilities within the next financial year. To the extent not already disclosed in accordance with paragraphs 122 and 125 of

NZ IAS 1, where an entity prepares its financial statements on a going concern basis, and management is aware of events or conditions that may cast significant doubt on the entity’s ability to continue as a going concern, it shall disclose information about the significant judgements and assumptions made as part of its assessment of whether the going concern assumption is appropriate.

13 This Standard, or its individual disclosure requirements, shall be applied for annual reporting periods beginning on or after 1 July 2011. Early application is permitted. If an entity applies these amendments for an earlier period it shall disclose that fact. An entity must also adopt the relevant requirements of Amendments to New Zealand equivalents to International Financial Reporting Standards and Australian Accounting Standards (Harmonisation Amendments) for the same period.

14 Amendment to FRS-44, issued in June 2011, inserted paragraph 2A. An entity shall apply that amendment for annual periods beginning on or after 1 July 2011. Early application is permitted.

15 Framework: Tier 1 and Tier 2 For-profit Entities, issued in November 2012, amended extant NZ IFRSs by deleting any public benefit entity paragraphs, deleting any differential reporting concessions, adding scope paragraphs for Tier 1 and Tier 2 for-profit entities and adding disclosure concessions for Tier 2 entities. It made no changes to the requirements for Tier 1 entities. A Tier 2 entity may elect to apply the disclosure concessions for annual periods beginning on or after 1 December 2012. Early application is permitted.

16 Amendments to Prospective Financial Statements (Amendments to FRS-42), issued in August 2013, amended paragraph 2A. An entity shall apply that amendment for interim or annual periods beginning on or after 1 January 2014. Earlier application is permitted.

17 2014 Omnibus Amendments to NZ IFRSs, issued in December 2014, amended paragraph 7. An entity shall apply that amendment for annual periods beginning on or after 1 April 2015. Earlier application is permitted.

18 Amendments to For-profit Accounting Standards as a Consequence of XRB A1 and Other Amendments, issued in December 2015, amended terminology for consistency with terminology used in XRB A1 and paragraphs 3, 5 and 7, deleted paragraph 6 and its related heading and added paragraphs RDR 5.1 and RDR 7.1. An entity shall apply those amendments for annual periods beginning on or after 1 January 2016. Earlier application is permitted.

19 2019 Omnibus Amendments to NZ IFRS, issued in September 2019, added paragraph 6.1 and the related heading and deleted paragraphs 12.1–12.10, the related heading and Appendix A. An entity shall apply those amendments for annual periods beginning on or after 1 January 2020. Earlier application is permitted.

20 Going Concern Disclosures (Amendments to FRS-44), issued in August 2020, added paragraphs 12A.1–12A.2 and the related heading. An entity shall apply those amendments for annual periods ending on or after 30 September 2020. Earlier application is permitted.

Disclosure of Fees for Audit Firms’ Services

21 The amending Standard Disclosure of Fees for Audit Firms’ Services (Amendments to FRS-44), published in May 2023, amended paragraphs 8.1 and 8.2 and the preceding heading and added paragraphs 8.3–8.36 and the related headings.

22 An entity applying the amendments in this amending Standard shall provide comparative information in respect of the preceding accounting period.

23 An entity shall apply these amendments in accordance with the commencement and application date provisions in paragraphs 24–26. An entity that applies these amendments to an ‘early adoption accounting period’ shall disclose that fact.

When amending Standard takes effect (section 27 Financial Reporting Act 2013)

24 The amending Standard takes effect on the 28th day after the date of its publication under the Legislation Act 2019. The amending Standard was published on 18 May 2023 and takes effect on 15 June 2023.

Accounting period in relation to which standards commence to apply (section 28 Financial Reporting Act 2013)

25 The accounting periods in relation to which this amending Standard commences to apply are:

-

for an early adopter, those accounting periods following, and including, the early adoption accounting period.

-

for any other reporting entity, those accounting periods following, and including, the first accounting period for the entity that begins on or after the mandatory date.

26 In paragraph 25:

early adopter means a reporting entity that applies this amending Standard for an early adoption accounting period.

early adoption accounting period means an accounting period of the early adopter:

-

that begins before the mandatory date but has not ended or does not end before this amending Standard takes effect (and to avoid doubt, that period may have begun before this amending Standard takes effect); and

-

for which the early adopter:

-

first applies this amending Standard in preparing its financial statements; and

-

discloses in its financial statements for that accounting period that this amending Standard has been applied for that period.

mandatory date means 1 January 2024.

This Basis for Conclusions accompanies, but is not part of, FRS-44.

Introduction

BC1 This Basis for Conclusions summarises the New Zealand Accounting Standards Board’s (NZASB’s) considerations in amending FRS-44. The FRSB Basis for Conclusions on FRS-44 sets out the matters considered when FRS-44 was first issued in 2011.

2019 Omnibus amendments to NZ IFRS

IFRS issued but not yet effective

BC2 Although the NZASB considers and issues the New Zealand equivalent to a new IFRS as soon as possible after the IASB issues the standard, the NZASB acknowledged that there may be times when an entity’s reporting date falls between the date of the IASB issuing the IFRS and the NZASB issuing the equivalent NZ IFRS. Under these circumstances, a Tier 1 for-profit entity applying NZ IFRS would not be able to assert compliance with IFRSs unless it made the disclosures required by paragraphs 30 and 31 of IAS 8 in addition to the disclosures required by NZ IAS 8.

BC3 To ensure that Tier 1 for-profit entities applying NZ IFRS are able to simultaneously assert compliance with IFRSs, 2019 Omnibus Amendments to NZ IFRS added paragraph 6.1 to require that, if an IFRS has been issued by the IASB but the equivalent NZ IFRS has not yet been issued by the XRB, an entity is required to disclose the information in paragraphs 30 and 31 of NZ IAS 8 in relation to that IFRS.

Elements of service performance

BC4 When FRS-44 was first issued in 2011 it specified the elements of a statement of service performance and required that a for-profit entity presenting a statement of service performance describe and disclose its outputs. In 2019 the NZASB deleted this section of FRS-44 (paragraphs 12.1–12.10 and Appendix A) for the following reasons.

-

The requirements in FRS-44 are no longer consistent with some legislative requirements for some public sector entities to establish and report against targets and performance measures. Some legislation is now less prescriptive regarding the terminology to be used by an entity in reporting targets and performance measures.

-

In addition, the requirements in FRS-44 are no longer consistent with the requirements in the PBE Standard dealing with service performance reporting. PBE FRS 48 Service Performance Reporting (issued in 2017) establishes principles and requirements for Tier 1 and 2 public benefit entities to present service performance information, but does not require that the terms inputs, outputs and outcomes be used.

Going concern disclosures

BC5 In June 2020 the NZASB issued ED 2020-2 Going Concern Disclosures (Proposed amendments to FRS-44). The NZASB noted that the COVID-19 pandemic in 2020 resulted in significant business disruption and uncertainties for many entities and led to an increased interest in going concern disclosures. The NZASB was of the view that more specific going concern disclosure requirements would help preparers of financial statements when applying existing disclosure requirements to provide relevant and transparent information to investors, lenders and other users of those financial statements in these circumstances, both in the current environment and in the future. The NZASB considered that users had an increased need for information about going concern assessments at this time. The NZASB also noted that there was diversity in practice in the level of information provided by entities and was of the view that users would benefit from more consistent disclosure.

BC6 The NZASB considered that the matter was of sufficient importance, and users’ need for information sufficiently urgent, to propose New Zealand-specific disclosures. Constituents were broadly supportive of the proposals, although some would have preferred that the matter be addressed by international bodies. The NZASB finalised these amendments in August 2020.

Fees for audit firms’ services

BC7 In June 2022 the NZASB issued ED 2020-9 Disclosure of Fees Paid to Audit Firms (Proposed amendments to FRS-44) to enhance the existing requirements concerning the disclosure of information about fees incurred by the reporting entity9 during the reporting period for:

-

the audit or review of the entity’s financial statements; and

-

other types of service provided by the entity’s audit or review firm.

BC8 The enhanced disclosures were proposed in response to concerns raised by key stakeholders about the inadequacy and inconsistency of information disclosed in general purpose financial statements about the nature and fees incurred for non-audit services provided by an entity’s audit or review firm.

BC9 The NZASB noted that the provision of non-audit services by an entity’s audit or review firm is often seen by users as a key indicator of possible threats to auditor or reviewer independence. However, the NZASB also noted that the provision of non-audit services is just one of several factors that should be considered by those charged with governance when assessing auditor or reviewer independence.

BC10 The NZASB agreed that the objective of the enhanced disclosures was not to provide users with all the information necessary to enable them to assess auditor independence, because those charged with governance have the responsibility for performing this assessment. In addition, the auditor’s report, issued as a result of a financial statement audit or review engagement, is required to include a statement that the auditor or reviewer is independent of the entity in accordance with the relevant professional and ethical standards.

BC11 In response to concerns raised by key stakeholders noted in BC8, the NZASB agreed the disclosure objective should be to provide information that will assist users of general purpose financial statements to assess the extent to which non-audit services have been provided by the entity’s audit or review firm in the reporting period.

BC12 The NZASB also agreed the disclosure objective was not to provide users with information about all relationships the audit or review firm may have with the reporting entity. The auditor or reviewer may have other relationships with the reporting entity in addition to those that arise from the provision of non-audit services. The auditor’s report, issued as a result of a financial statement audit or review engagement, is required to include a statement as to the existence of any relationship (other than that of auditor or reviewer) which the auditor or reviewer has with, or any interest which the auditor or reviewer has in, the entity or any of its subsidiaries.

BC13 The NZASB acknowledged that under applicable professional and ethical standards, auditors and audit firms are prohibited from providing certain non-audit services under certain circumstances. The NZASB noted the enhanced disclosures are not intended to provide guidance on when it is appropriate for certain types of non- audit services to be provided by an entity’s audit or review firm. Instead, the enhanced disclosures are intended to provide increased transparency and consistency of reporting when a reporting entity has incurred fees for non-audit services in the reporting period.

BC14 The NZASB noted the Australian Accounting Standards Board (AASB) has an ongoing project on Auditor Remuneration which is considering the introduction of similar enhanced disclosures. In December 2021, the NZASB agreed to develop, and issue proposed amendments ahead of AASB pronouncements on this topic. This decision was based on the uncertainty concerning when the AASB will be in a position to finalise its proposals and the need to respond to calls for improved disclosures from New Zealand stakeholders. The NZASB acknowledged the intention to harmonise the enhanced disclosure requirements with Australia in the future.

BC15 The NZASB considered whether the amendments should also include proposals concerning the disclosure of information about audit tenure. The Board acknowledged this provided important information for users when considering risks to auditor independence but agreed not to propose disclosure requirements about audit tenure at this time. The Board will continue to follow developments in Australia and internationally on this matter.

BC16 Constituents were broadly supportive of the proposed enhanced disclosure. However, some constituents recommended refinements and improvements to the proposals. The key areas where the NZASB agreed to make changes to the proposals based on constituents’ feedback are explained below.

Classification of agreed-upon procedures engagements

BC17 The proposed disclosure requirements did not specifically refer to agreed-upon procedures engagements. Some constituents recommended clarifying the category in which such engagements should be classified to promote consistent application. It was also noted that some agreed-upon procedures are consistent with the description of ‘audit or review related services’ and should be classified in that category when this is the case.

BC18 In response to constituents’ feedback, the NZASB agreed to:

-

Extend the category ‘other assurance services’ to ‘other assurance services and other agreed-upon procedures engagements’; and

-

Specify that an agreed-upon procedures engagement is classified as ‘audit or review related services’ when the nature of the engagement is consistent with the description of that category – otherwise, the engagement is classified as ‘other assurance services and other agreed-upon procedures engagements’.

BC19 The NZASB acknowledges that for some types of agreed-upon procedures engagements, judgement may be required in assessing whether the most appropriate category is ‘audit or review related services’ or ‘other assurance engagements and other agreed-upon procedures engagements’. However, possible inconsistencies in classification are expected to be mitigated by the requirement to disclose the nature of the services included within each category.

BC20 Furthermore, to mitigate the impact of judgement mentioned in paragraph BC19, the NZASB decided to require entities to:

-

categorise each type of service classified within ‘audit or review related services’ as an assurance engagement, an agreed-upon procedures engagement, or another non-assurance engagement; and

-

categorise each type of service classified within ‘other assurance engagements and other agreed-upon procedures engagements’ as an assurance engagement, or an agreed-upon procedures engagement.

Clarifying the classification of assurance engagement

BC21 Some constituents noted that confusion may arise when determining whether an assurance engagement should be classified as ‘audit or review related services’ or as ‘other assurance engagements’. In response, the NZASB clarified that an assurance engagement whose nature is consistent with the description of the ‘audit or review related services’ category is classified in that category, otherwise it is classified as ‘other assurance services and other agreed-upon procedures engagements’.

BC22 The NZASB acknowledges that for some assurance engagements, judgement may be required when determining which of the two abovementioned categories is the most appropriate. However, as noted above in paragraph BC19, possible inconsistencies in classification are expected to be mitigated by the requirement to disclose the nature of the services included within each category, and by the additional disclosure requirements described in paragraph BC20.

Removal of the proposed disclosure requirements about mitigating risk to auditor independence in certain circumstances

BC23 The proposed amendments included a requirement to disclose information about how the entity identifies, evaluates, and mitigates the possible threats to auditor or reviewer independence that might arise from the provision of ‘taxation service’ or ‘other services’ by the audit or review firm.

BC24 Several respondents expressed concerns about this proposal. They noted that professional and ethical standards require auditors and reviewers to ensure that they are independent of the audit or review client. However, the proposed disclosure may imply that the responsibility for ensuring auditor independence lies fully with the reporting entity, and may confuse users of financial statements as to the responsibilities of the auditor with respect to independence as compared to the responsibilities of the entity. Some respondents considered information about mitigating possible threats to auditor independence more appropriately belongs outside of the general purpose financial statements (e.g. elsewhere in the annual report, together with other corporate governance information). Another concern was that the disclosure requirement would give rise to ‘boiler plate’ disclosures that would not be useful to users of general purpose financial statements. Discussion with constituents also highlighted that guidance issued by financial market regulators recommends providing information in the annual report in relation to mitigating possible threats to auditor independence.

BC25 After considering constituents’ feedback, the NZASB agreed not to include disclosure requirements about how an entity manages possible threats to auditor independence when certain services are provided.

Disclosure concessions for entities in Tier 2

BC26 The proposals included disclosure concessions for Tier 2 entities only with respect to the proposed disclosure relating to the mitigation of auditor or reviewer independence (see paragraph BC23 above). However, some constituents recommended additional concessions for Tier 2 entities – to ensure that the cost of providing the disclosure does not outweigh the benefits, given that Tier 2 entities do not have public accountability.

BC27 In response to constituents’ feedback, the NZASB agreed that Tier 2 entities be required to disclose only:

-

the total fees incurred for the audit or review of the entity’s financial statements; and

-

the total fees incurred for other types of service provided by the entity’s audit or review firm (without requiring further disaggregation), together with a general description of these services.

BC28 The NZASB acknowledges that before Disclosure of Fees for Audit Firms’ Services was issued, this Standard did not require Tier 2 entities to provide any disclosures relating to fees paid to audit firms. However, the disclosure requirements for Tier 2 entities described in paragraph BC 27, which were introduced by Disclosure of Fees for Audit Firms’ Services, are consistent with the requirements for Australian Tier 2 entities as set out in AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities. The NZASB considers such alignment to be appropriate.

Disclosure of significant fees incurred after the end of the reporting period

BC29 The proposed disclosure requirements referred to the disclosure of fees incurred during the reporting period. However, some constituents recommended that entities be required to disclose fees incurred for services provided by the audit or review firm after the end of the reporting period, but before the audit or review report is signed – as well as services not yet provided by the audit or review firm, but for which the audit or review firm has been engaged before the audit or review report is signed. The constituents acknowledged that such fees would not be recognised as expenses in profit or loss in the period for which the financial statements are prepared. However, the constituents noted that disclosure of such fees is relevant and important for users’ assessment of the extent of non-audit services provided by the audit or review firm, and the assessment of auditor independence with respect to the current period financial statements audit or review.

BC30 In response to the feedback above, the NZASB considered whether to include a requirement to disclose significant fees for services that the audit or review firm has been engaged to provide (including engagements entered into up until the date when the audit or review report is signed), but for which fees were not incurred during the reporting period.

BC31 The NZASB decided not to include the disclosure requirement described in paragraph BC30 above, for the following reasons.

-

The effort of complying with a requirement to disclose (significant) fees incurred/engaged for after the reporting may outweigh the benefits, given that this information is already expected to be included in the auditor’s report;

-

The enhanced disclosures introduced by Disclosure of Fees for Audit Firms’ Services are not intended to provide users with all information required for assessing auditor independence;

-

Disclosures in financial statements generally focus on the current reporting period (together with comparative information).

-

There are existing accounting standards that address the disclosure of material events after the reporting period.

Application of materiality considerations

BC32 Feedback on the ED included an observation that fees for services provided by the entity’s audit or review firm other than for the audit or review of the financial statements are often low in value, and therefore, such fees may often not be disclosed due to materiality considerations. However, NZ IAS 1 Presentation of Financial Statements notes that “materiality depends on the nature or magnitude of information, or both.”

BC33 It is possible that a fee incurred for a non-audit service provided by the entity’s audit firm may be low in value, but the nature of the service may be such that information about the service and the related fee meets the definition of materiality in NZ IAS 1. That is, it may be that “omitting, misstating or obscuring it could reasonably be expected to influence decisions that the primary users of general purpose financial statements make on the basis of those financial statements, which provide financial information about a specific reporting entity”.

BC34 Given the importance of auditor independence to users of the financial statements, and the connection between the assessment of auditor independence and the fees incurred for non-audit services provided by the entity’s audit firms, it is particularly important to consider the nature of the service – not only the magnitude of the fee – when determining whether to provide the disclosures required by this Standard.

BC35 The NZASB finalised the amendments in April 2023.

This Basis for Conclusions accompanies, but is not part of, FRS-44.

Introduction

BC1 This Basis for Conclusions summarises the Financial Reporting Standards Board’s (FRSB) considerations in reaching its conclusions on FRS-44 New Zealand Additional Disclosures (FRS-44) in 2010. It also provides a context of the FRSB’s decision about harmonising the disclosure requirements. It focuses on the issues that the FRSB considers to be of greatest significance. Individual FRSB members gave greater weight to some factors than others.

Location of additional disclosures

BC2 The FRSB and the Australian Accounting Standards Board (AASB) discussed the merits of locating the additional domestic disclosure requirements in a separate disclosure standard compared with locating them within topic-based standards, which is the current practice. Some members supported a separate disclosure standard largely on the basis that it would facilitate the topic-based standards being identical to IFRSs. Other members expressed a preference for locating additional disclosures within topic-based standards for ease of use. On balance, the Boards decided to locate the additional disclosures in separate disclosure standards on the basis that they view bringing the wording of New Zealand and Australian Standards closer to IFRSs as one of the greatest benefits of the trans-Tasman Convergence project.

Background

BC3 On 20 August 2009 a Prime Ministerial Joint Statement of Intent outlined a range of trans-Tasman outcome proposals, the benefits to be achieved or problems to be solved, and the relevant timeframes. The revised Memorandum of Understanding between the Government of New Zealand and the Government of Australia on the Coordination of Business Law was signed by Hon Simon Power and Hon Chris Bowen on 23 June 2010. This Memorandum recognises the Single Economic Market Outcomes Framework endorsed by the Prime Ministers in their Joint Statement of Intent on 20 August 2009.

BC4 The specific outcome proposals relevant to FRS-44 relate to enabling for-profit entities to prepare only one set of financial statements that would be recognised in both jurisdictions. The Joint Statement of Intent noted that such an outcome would allow for a reduction in compliance costs for entities operating across the Tasman and it would support trans-Tasman investment through the consistency of financial statements.

BC5 The FRSB and the AASB jointly issued FRSB ED 121/AASB ED 200A and FRSB ED 122/AASB ED 200B for the purpose of harmonising each jurisdiction’s standards with source IFRSs to eliminate many of the differences between the standards in each jurisdiction relating to for-profit entities applying IFRSs as adopted in Australia and New Zealand.

BC6 FRS-44 contains New Zealand-specific disclosure requirements which have been relocated from existing NZ IFRSs because they were considered by the FRSB to remain important in the New Zealand environment despite the harmonisation objective.

BC7 To achieve the objective of the Prime Ministerial Joint Statement of Intent, in instances where AASB 1054 Australian Additional Disclosures contains a similar disclosure to FRS-44, the wording of those disclosures is harmonised to enable consistent application of those common disclosures in both jurisdictions.

BC8 The specific paragraphs below explain the FRSB’s rationale for requiring the specific disclosures.

Compliance with applicable financial reporting standards

BC9 The FRSB has retained the requirement to disclose in the entity’s interim financial statements that those statements have been prepared in accordance with NZ IAS 34 Interim Financial Reporting. This is an important feature of New Zealand’s financial reporting environment and provides a level of assurance to the users of the entity’s interim financial report.

Audit fees (paragraphs 8.1–8.2)

BC10 The AASB and the FRSB have relocated and amended the audit fee disclosure requirements contained in AASB 101 Presentation of Financial Statements and NZ IAS 1 Presentation of Financial Statements to their respective separate disclosure Standards and harmonised the disclosure requirements across both jurisdictions.10

BC11 The AASB and the FRSB consider that the disclosure of audit fees is a matter of accountability and, given that the accountability environment is similar in both jurisdictions, they should have the same audit fee disclosure requirements. The Boards also took the opportunity to simplify the disclosure requirements on the basis that in recent times both preparers and users have indicated that disclosures in financial statements have become overly complex.

BC12 The AASB and FRSB noted the usefulness of the notion of ‘related practice’ in audit fee disclosures in AASB 101 and decided to incorporate a similar notion that is common to both jurisdictions in the harmonised disclosures. Accordingly, the Boards decided to include the notion of ‘network firm’ from APES 110 Code of Ethics for Professional Accountants issued by Accounting and Professional Ethical Standards Board (APESB) (February 2008) and Code of Ethics: Independence in Assurance Engagements issued by New Zealand Institute of Chartered Accountants (NZICA) (September 2008). The Boards also decided not to define or provide explanatory material for ‘network firm’ on the basis that the notion is generally understood and preparers and auditors could refer to the relevant APESB and NZICA pronouncements.

BC13 The AASB and FRSB note that disclosures are made in the context of the scope of the entity reporting. Accordingly, in the case of a group, disclosures made in accordance with paragraph 8.1 would include fees paid by the parent and its subsidiaries for each of the parent and its subsidiaries.

BC14 For New Zealand entities the harmonised audit fee disclosure may require more information than was required by the previous disclosure requirements. The FRSB considers that the benefits of harmonisation outweigh the cost of requiring any additional disclosure requirements.

Imputation credits (paragraphs 9.1–9.4)

BC15 The AASB and the FRSB have relocated the imputation credit disclosure requirements contained in AASB 101 and NZ IAS 12 Income Taxes to their respective separate disclosure Standards and to harmonise the disclosure requirements across both jurisdictions.

BC16 The AASB and the FRSB noted that Australia and New Zealand are among a limited number of jurisdictions that have an imputation tax regime and acknowledge the decision usefulness of information about imputation credits to users of financial information. Accordingly, the AASB and the FRSB decided that these additional disclosure requirements should be retained.

BC17 Given that both jurisdictions have additional disclosure requirements about imputation credits, and that the imputation regimes in each jurisdiction are highly similar, the Boards have harmonised the wording across both jurisdictions. The Boards also took the opportunity to simplify the disclosure requirements on the basis that in recent times both preparers and users have indicated that disclosures in financial statements have become overly complex.

Reconciliation of net operating cash flow to profit (loss) (paragraph 10)

BC18 The AASB and FRSB have relocated the requirement to disclose a reconciliation of net cash flows from operating activities to profit or loss when an entity uses the direct method to present its statement of cash flows [that were contained in AASB 107 Statement of Cash Flows and NZ IAS 7 Statement of Cash Flows] to their respective separate disclosure standards and to harmonise the disclosure requirements across both jurisdictions.

BC19 The Boards, in forming the view to retain the requirement for a reconciliation of net cash flows from operating activities to profit or loss, acknowledged the weight of comments received from constituents who opposed the proposal to remove this requirement.

BC20 The Boards note that the IASB has recently considered requiring a reconciliation of net cash flows from operating activities to profit or loss in the context of its Financial Statement Presentation project.

Prospective financial statements (paragraphs 11.1–11.2)

BC21 The FRSB has retained the requirement to present a comparison of the prospective financial statements with the historical financial statements where the entity has published general purpose prospective financial statements for the period of the financial statements. The FRSB considers that the requirement is an important feature of New Zealand’s financial reporting environment. The FRSB noted that the rationale for providing such a comparison is set out in FRS-42 Prospective Financial Reporting.

Elements of statements of service performance (paragraphs 12.1–12.10)

BC22 The FRSB has retained the guidance relating to the elements of statements of service performance because statements of service reporting are a unique feature of New Zealand’s financial reporting environment.11

Summary of main changes from the Exposure Draft

BC23 The main change from those proposed in ED 122 is the requirement to present a reconciliation of operating cash flows to profit or loss has been included in this Standard. In ED 121 the FRSB proposed to remove the requirement to present a reconciliation of operating cash flows to profit or loss. The Boards, in forming the view to retain the requirement to present a reconciliation of cash flows from operating activities to profit or loss, acknowledged the weight of comments received from constituents who opposed the proposal to remove this requirement. The Boards note that the IASB has recently considered requiring a reconciliation of cash flows from operating activities to profit or loss in the context of its Financial Statement Presentation project.11